Looking At: Everything But the War

Estimated reading time: 6 minutes

Topics From the Bench

Markets seem to be tired of worrying about the war, with the S&P 500 surpassing its pre-war levels on Monday and the Nasdaq posting +14% returns in the last 10 trading days. Although the war is not over and no definitive resolution has been reached, investors seem satisfied with the momentum toward resolution for the moment.

So let’s dig into some other topics that are important in markets this month.

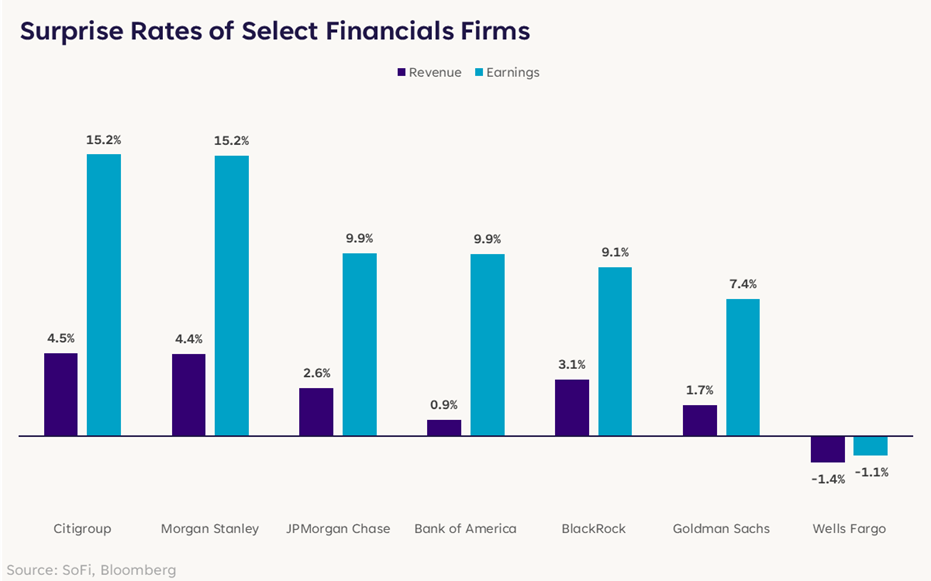

Banks Beat

We’re grateful to have earnings to talk about right now. Things are looking good so far and this is one of the drivers of current positive sentiment among investors.

As always, Q1 earnings season kicked off in earnest with the big banks reporting results. They usually set the tone, and this time around the tone is quite positive, even if some of their stock prices didn’t reflect that level of enthusiasm.

Of the major financial companies that have reported so far – Goldman Sachs, BlackRock, Wells Fargo, JPMorgan, Citigroup, Bank of America, and Morgan Stanley – all but Wells Fargo beat earnings and sales estimates.

Commentary from C-suites are followed closely by market participants for indications of the business environment. Their sentiment was generally strong, although most did acknowledge ongoing geopolitical risks and possible growth concerns if the conflict drags on. But it would be weird if they didn’t say something like that.

Bank earnings are certainly not the main story driving markets higher right now, but the fact that they came in relatively strong – and frankly, that they didn’t come in weak – serves as a solid foundation for the rest of the earnings season.

Also worth noting, in recent weeks we’ve pointed out that the Financials sector can serve as convincing validation for market rallies. A rally that doesn’t include the banks is to be questioned, IMO. So far, this one does.

An Odd, But Accurate, Bellwether

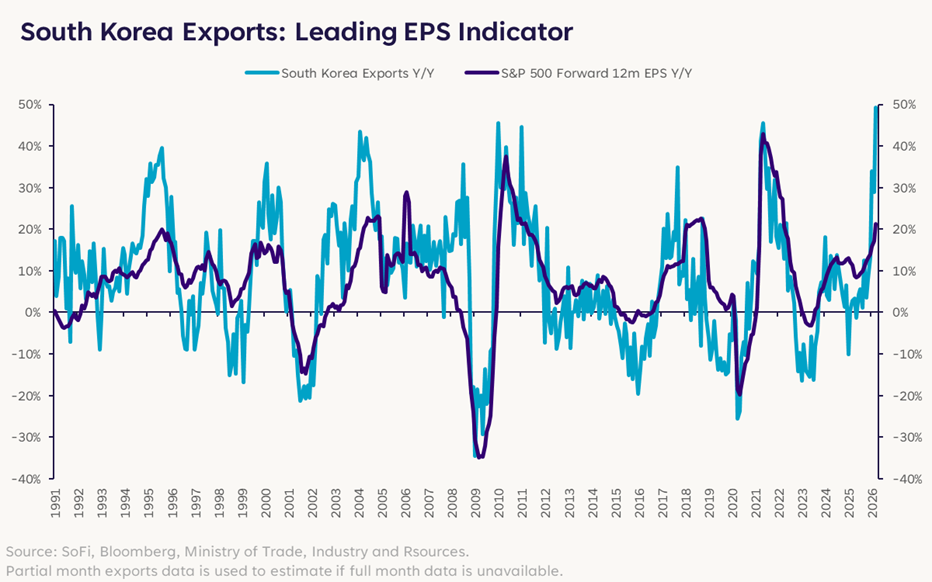

Earnings season is still young, with only 30 S&P companies having reported as of Wednesday morning, but the outlook is strong. Bottom-up estimates are calling for 11.3% earnings growth for Q1 and 16.9% for the full year, which is strong relative to most comparisons. If that materializes, markets will have the fundamental support they need and investors will remain optimistic.

One of the interesting correlations in markets is between South Korean exports and U.S. earnings growth. Specifically, South Korean exports tend to lead U.S. forward earnings growth by roughly one month, largely due to the technology ordering cycle. South Korea is the world’s largest producer of memory chips, and when orders go up, it typically means technology giants are gearing up for increased demand and higher revenue.

Given growth in AI and the CapEx spending boom that’s resulted, this metric is particularly sensitive and showing very strong trends.

By this metric alone, it appears that there is much more upside for earnings growth and the double-digit growth expectations for 2026 are warranted.

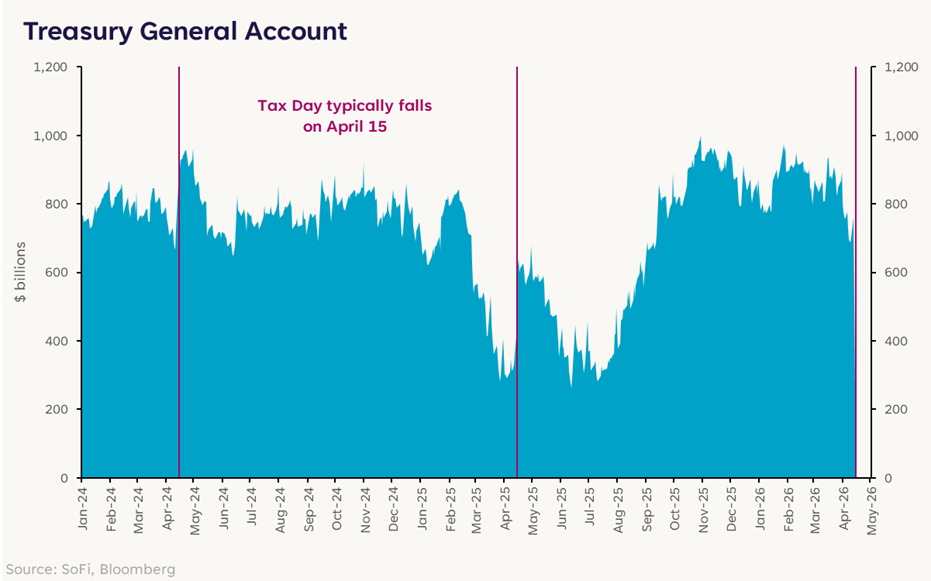

Tax Week Wonkiness

Outside of earnings and the war, the other major news this week is the U.S. tax deadline. The interesting piece of this to watch is that as the Treasury receives tax payments, liquidity in markets tends to get squeezed temporarily and some volatility can ensue. This is usually expected by the Fed and institutional investors and is not something to fear, per se, but it can cause some wonky moves for a couple weeks.

Without getting too far into the weeds, as tax receipts come in, the Treasury’s account at the Fed (Treasury General Account or TGA) grows. That growth is offset by a reduction in bank reserves, which effectively pressures funding markets in the near term.

This is not a warning, and it’s not a guarantee that volatility will rise. It’s simply a force to be aware of that could affect commentary from the Fed in coming meetings. The Fed recently announced that it would reduce its monthly bond buying from $40b to $25b, which though well-telegraphed, is also a reduction in liquidity support.

Markets can likely withstand both of these forces, but if liquidity gets uncomfortable, I’d expect the Fed to change its tune… even with a new Fed chair in the seat.

All in all, the war is still the most important force in markets. But its headline dominance doesn’t eliminate the other drivers under the surface right now. Stay vigilant, but stay invested.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.