Decoding Markets: A Fragile Ceasefire

Estimated reading time: 6 minutes

This week all eyes will be on the Federal Reserve’s outlook on interest rates.

Markets have spent the last few weeks trading on the possibilities of what could happen: oil and gas shortages, rising food costs, so-called demand destruction (aka we consumers spend less), and more. But what actually ends up happening will be the final arbiter of market direction. With the first-quarter earnings season upon us, there’s a lot to unpack.

The Illusion of Calm

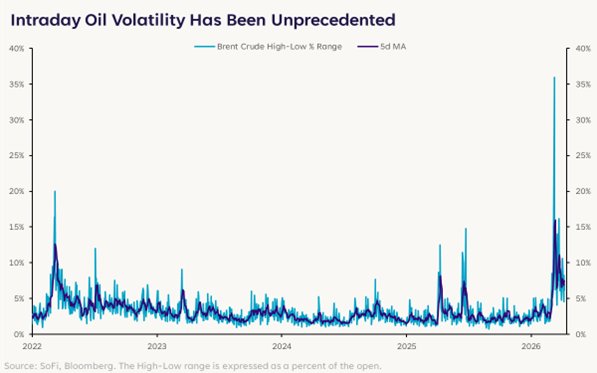

The war in the Middle East is, of course, at the forefront of the market’s mind, especially considering the sudden news of a two-week ceasefire between the U.S. and Iran late Tuesday. At first glance, a pause in the conflict feels like a much-needed sigh of relief for oil markets, which have been averaging intraday swings of nearly 10 percentage points since the war began. That level of volatility eclipses what we saw when Russia invaded Ukraine in 2022.

Not is all as it seems, however. If the initial version of the Pakistan prime minister’s social media post is any indication, the pause – though officially brokered by Pakistan – may have been dictated by the U.S. behind the scenes. There are two things to note from this:

- If true, this telegraphs that the U.S. is concerned about the economic and political pain stemming from the war, suggesting that the famous “Trump Always Chickens Out” (TACO) trade is alive and well. Over the past year, investors have grown to love the TACO theme, feeling comforted by signs that the president will backtrack if his moves create too much market upheaval. (Somewhat ironic given that it’s the anniversary of last year’s tariff TACO).

- If the U.S. was chiefly responsible for the Pakistani ceasefire proposal (which came just hours before the president’s self-imposed deadline to destroy a “whole civilization,”) that suggests a lack of progress on negotiations and a desire to walk back the threat. In other words, this development just kicks the can further down the road.

As we write this on Wednesday, news of disagreements is already trickling through. There have been additional attacks on energy infrastructure in the region, and the Iranians are weighing further action in response to what they describe as Israeli ceasefire violations.

Even if some form of ceasefire holds, the reality on the water remains grim. News reports suggest that only 10 to 15 ships would be allowed to pass through the Strait of Hormuz during this ceasefire. That would be 80%-90% below the pre-war flow through this critical oil chokepoint – not even close to enough to resolve the disruption in global oil supply.

The message: Given how far apart negotiations appear, it’s hard to imagine a permanent agreement materializing anytime soon. Further volatility seems inevitable.

Earnings in the Fog of War

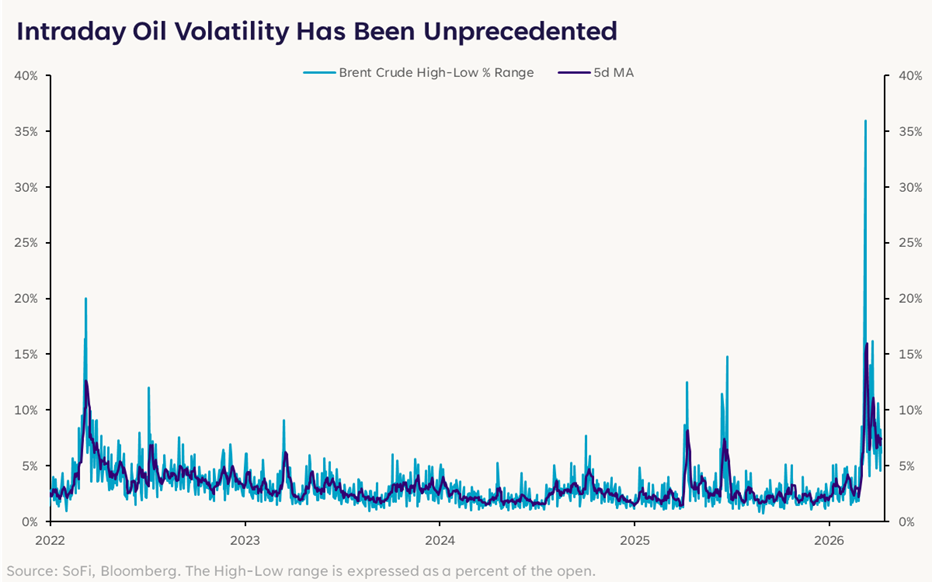

Again, what ultimately matters is what actually happens. It’s way too early to tell, but so far, Wall Street analysts are surprisingly sanguine about U.S. corporate profits. Full-year earnings revisions have been pretty muted since the war began, and estimates for the Information Technology, Energy, and Materials sectors have been revised markedly higher.

The throughline here is pretty intuitive: Stocks that are sensitive to commodity prices (like the Energy and Materials sectors) are benefiting from the direct flow-through of supply and demand. But it’s less clear for other sectors. Mixed revisions for other sectors shouldn’t be taken as a sign that analysts expect no impact from the war. It’s just that the economic consequences are hard to price in, particularly for the end consumer. It’s the fog of war, literally.

Eventually, prolonged oil supply disruptions would act as a stagflationary force – first as a tax at the pump, and then as a dampener of spending on other goods and services. Normally, investors would rely on corporate management teams during earnings calls to provide clarity and forward guidance. But given how rapidly the geopolitical chessboard changes week to week, it’s hard to imagine executives sticking their necks out with confident forecasts.

The Spending Bender Continues

Even with war dominating the front pages, artificial intelligence remains the gravitational center of the stock market. Recent chatter surrounding Anthropic’s new “Mythos” model – and the accompanying worries that AGI (Artificial GeneralIntelligence) will become too powerful – show that the technological revolution continues with no signs of slowing down.

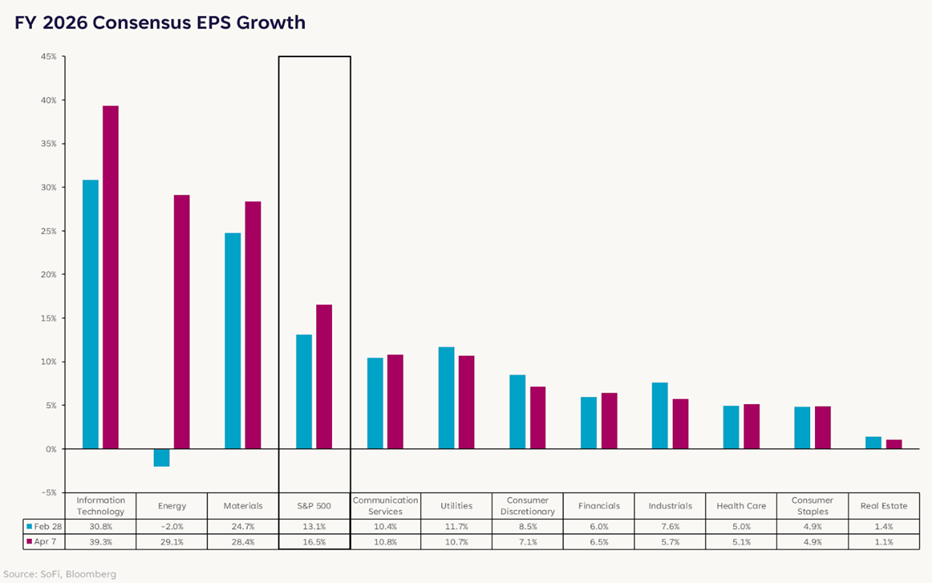

The perceived cost of falling behind in AI is existential, so companies are engaging in an arms race to win the spoils of a new future. Hyperscaler capital expenditure (CapEx) estimates continue to get revised higher, with nearly $2.2 trillion in spending expected through 2028.

To put it bluntly, tech heavyweights aren’t going to stop investing in data centers, chips, and power infrastructure – regardless of what happens in the Strait of Hormuz. If lower consumer spending does shrink the economic pie, it’s hard to imagine the first effects would be felt in the tech space.

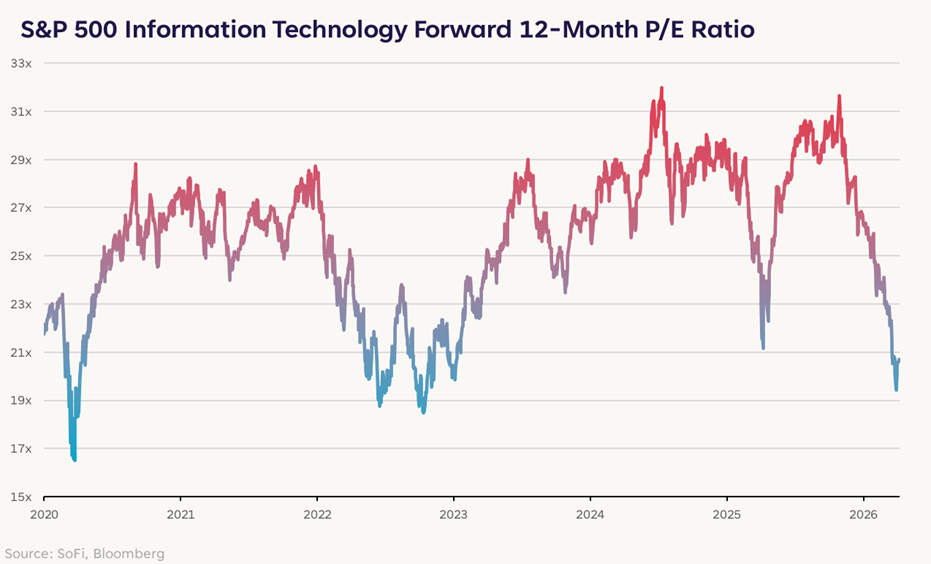

Even still, the recent bouts of market turbulence have caused the broader technology sector to rerate lower. P/E multiples in the space have compressed and are now sitting near their 2022 lows.

With valuations becoming much more digestible, tech could start commanding a lot more attention moving forward, especially if the ceasefire does in fact lead to a more durable peace in the region.

At the end of the day, while other sectors might enjoy a rotation in the sun, tech remains the market’s heavy lifter. It is very hard to imagine the broader indices making a sustained run back to all-time highs if the technology sector doesn’t participate.

While geopolitical tensions and the daily headlines of war will undoubtedly dictate trading action in the short term, the underlying trajectory of AI and tech remains a defining long-term driver for investors to watch.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.