Looking at: The Name Is Bond

Estimated reading time: 0 minutes

Pre-Existing Conditions

Investors usually assume that when bad stuff happens in the world, markets price that in. They also assume the reverse: When the news gets better, things unwind. Unfortunately, that’s not entirely true right now.

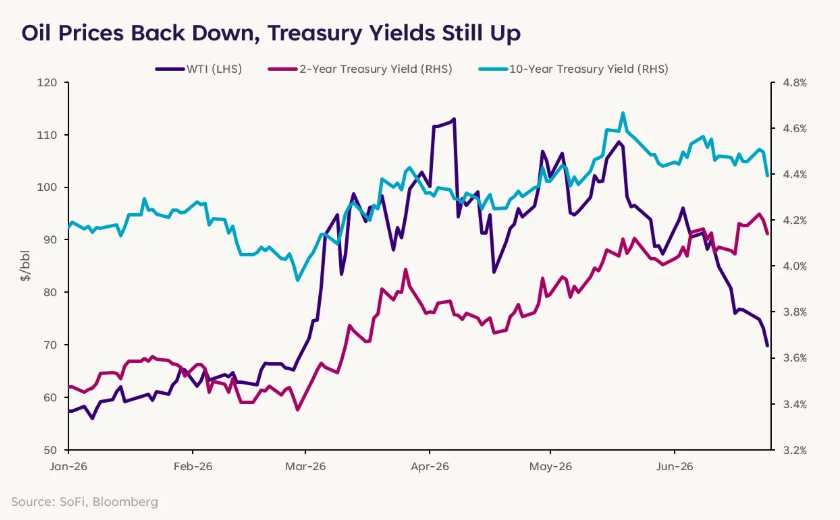

The recent peace agreement between the U.S. and Iran has restored a sense of order to global markets, at least for now. More tankers are able to get through the Strait of Hormuz, pushing crude oil prices back down to the low-$70/bbl range after being well above $100/bbl.

And yet, Treasury yields are still much higher than they were before the war. As of Wednesday’s close, the 2-year Treasury yield is at 4.15% (compared with 3.43%), while the 10-year yield is near 4.40% (compared with 4.00%.) When the oil shock hit, yields rose in part because investors expected inflation to accelerate. So shouldn’t the recent détente push them back down?

Things are almost never that simple in financial markets. And that might be even truer for the bond market and interest rates.

Inflation was elevated even before the war started. The inflation rate for core services excluding housing has been 1-2 percentage points above pre-pandemic levels for the last five years, and theoretically, that has little to do with the price of oil.

So in a sense, it might be less about recovering from the oil shock and more about realistically pricing in an inflationary backdrop that was already there.

Washington’s Fingerprints

Looking beyond the Middle East, Washington is also leaving its mark on things.

At Kevin Warsh’s first FOMC meeting as chairman of the Federal Reserve, he stressed the Fed’s “unambiguous and unanimous” commitment to getting inflation back to its 2% target. Investors who were looking for signs that Warsh may be more accepting of higher inflation were caught a bit off-guard by the hawkish tone.

He also rejected the idea of explicit forward guidance from the Fed, and as a rule of thumb less clarity from the Fed means more uncertainty for the path of interest rates. This uncertainty could manifest in the form of a higher term premium — investors demanding extra compensation for holding longer-term bonds amid increased risk. For now, however, the renewed commitment to fight inflation is offsetting this uncertainty.

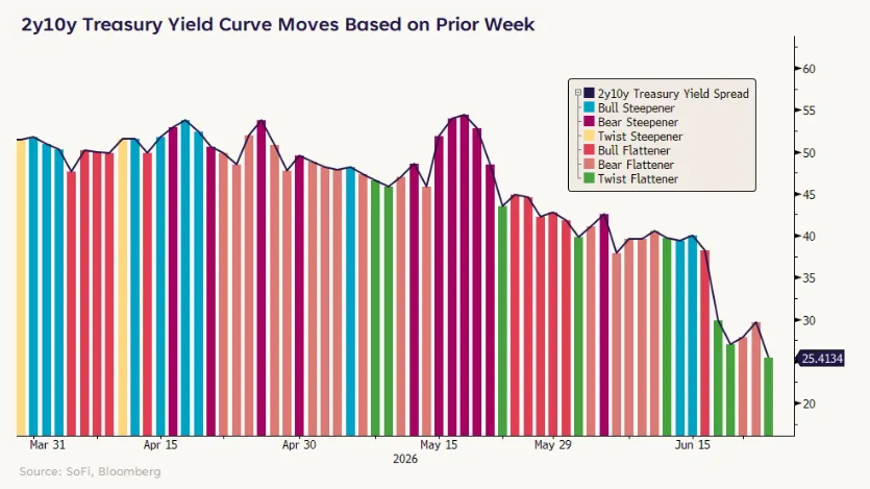

The hawkish posturing has contributed to both bear and twist flattening of the Treasury yield curve, where short-term rates rise faster than long-term rates rise (or even fall). In plain English: Investors believe the Fed will incrementally raise rates to fight inflation, but also see rates coming back down once those higher rates weigh on economic growth.

Simultaneously, the fiscal picture of the U.S. remains an ongoing concern. To fund the government, the Treasury Department has to issue debt (as any nation does), but debt issuance has ballooned because of the historic nature of the U.S. deficit. It’s more complicated than this, but all else being equal, more debt issuance means more Treasury supply, more supply means lower prices, and lower prices mean higher yields.

AI Borrowing Binge

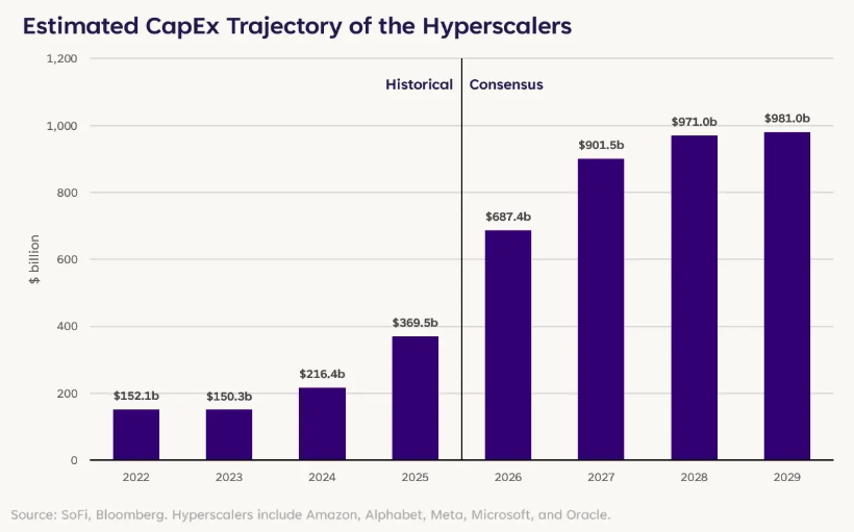

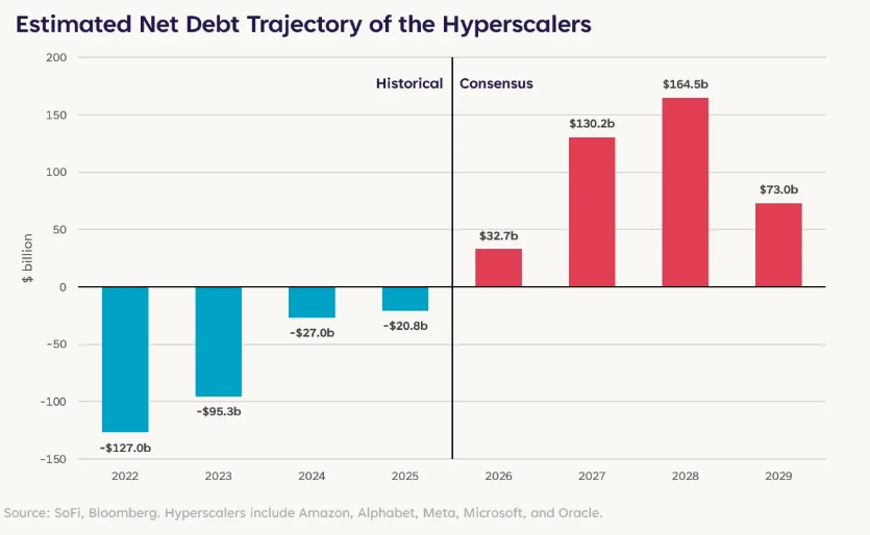

Similar to how Washington issues Treasurys to fund the government’s obligations, companies raise money to pursue opportunities. Right now the biggest opportunity is artificial intelligence, and the hyperscalers are rapidly scaling and building out AI infrastructure.

Since 2022, these mega-caps have allocated over $900 billion in capital expenditures and are projected to spend an additional $3.4 trillion through 2029.

But as the numbers get bigger and bigger, even the most profitable giants don’t have the free cash flow to cover everything. Analysts expect these companies to increasingly tap debt markets to fill in the gaps.

Just as more government debt tends to push Treasury yields higher, we can also expect more corporate debt to push corporate bond yields higher, widening credit spreads versus Treasurys.

Of course, there are differences between Treasurys and corporate bonds, but the pool of fixed-income investor dollars isn’t limitless, and more supply in one segment of debt markets can have an impact on other segments. This is why volatility in the Japanese bond market affected the global bond market a few months ago.

To state the obvious, a lot is going on and there’s a lot to digest: Uncertainty about inflation continues, we’re probably going to have less transparency from the Fed, and there will be more private sector borrowing as the infrastructure of the future is built. Varying market developments are competing for oxygen and tugging in different directions. How it shakes out remains to be seen, but expect the road to be bumpy.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

Crypto and Crypto ETF products are available only to members in eligible jurisdictions who have successfully completed the required assessments and maintain an appropriate risk profile.

This communication is not directed at, and is not intended for distribution to or use by, any person in the United Kingdom. It does not constitute a financial promotion for the purposes of Section 21 of the Financial Services and Markets Act 2000. This material is not available to any UK Person. By accessing, viewing, or relying on this communication, you represent and warrant that you are not a UK Person and that you are not located in the United Kingdom.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.