Looking At: A Pulse Check on the Economy

Estimated reading time: 6 minutes

Return of the Macro

We haven’t written about the macro environment much this year because market volatility and major geopolitical events have dominated the headlines. But now seems like a good time to do a check-in on the state of things in the U.S. economy. (Call it ‘Return of the Mack-ro’ for you 90s kids like me.)

As we try to determine whether things are good, bad, or otherwise, here are some areas to look at.

Jobs

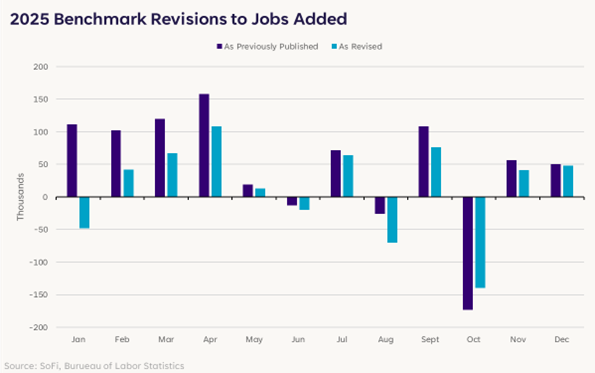

The most recent labor data was relatively positive, with 130k jobs added (vs. expectations for 65k) and an unemployment rate that fell from 4.4% to 4.3%. That’s encouraging and sends a message of stability or even strengthening, though it’s not the full picture.

In addition to the January data, the government also released revised numbers for the full year of 2025, and that showed that we added 862k fewer jobs than originally reported. That’s the largest downward revision since 2009.

Accounting for that data, the average jobs added per month last year was only 15k, which is lower than we’d prefer (or than most economists and the Fed, we’d suspect).

It’s safe to say that the labor market has cooled considerably in the last few years, and now we’re at a point where we need it to stabilize or strengthen slightly in order to maintain harmony in the economy. In order to prevent higher unemployment, we need to be adding more jobs on a monthly basis: The current ratio of open jobs to unemployed workers is 0.87, meaning there aren’t quite enough jobs to employ every person looking for work.

That’s why we’d call the state of the labor market fine, but not great. It’s weaker, but not to a point that shows conclusively negative things in the data. We just don’t have much of a buffer to absorb further weakening, so this is a piece of the macro environment that could become the main story very quickly if things continue slowing.

That said, immigration changes, tariff announcements, and government changes (i.e. DOGE cuts in October) made for some unique circumstances in 2025. If those dynamics affected the data, it’s possible we’ve already seen the bottom in the labor market and it could strengthen as the year progresses.

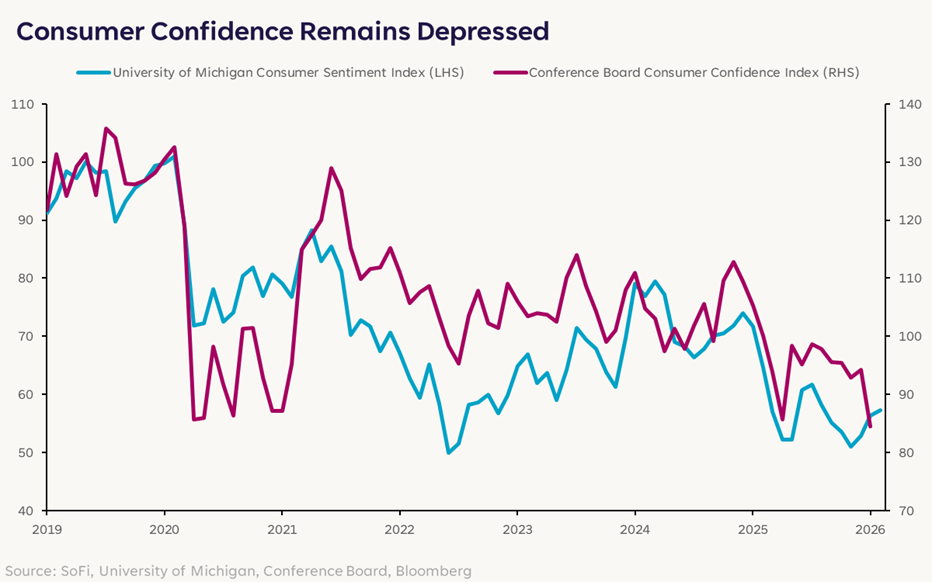

Consumer Sentiment

Given that consumer spending makes up roughly two-thirds of U.S. GDP, it’s important to have a pulse on how consumers are feeling. The two main metrics used to track this are the University of Michigan Consumer Sentiment index and Conference Board’s Consumer Confidence index.

The two surveys include different lines of questioning, with the University of Michigan’s skewing more towards inflation concerns and the Conference Board’s skewing more towards jobs. Both have been quite choppy in recent months.

Perhaps not surprisingly, the Conference Board’s measure has dropped more recently given the softer labor market picture. We have said for a while that the consumer will keep spending as long as the consumer is employed. But it’s worth noting that the consumer’s perception of the labor market also influences how much they are willing to spend.

The output of these surveys can change rapidly. If we’ve already seen the bottom in the labor market, we’d expect an improvement in the Conference Board index in coming months. And that could help calm investor fears.

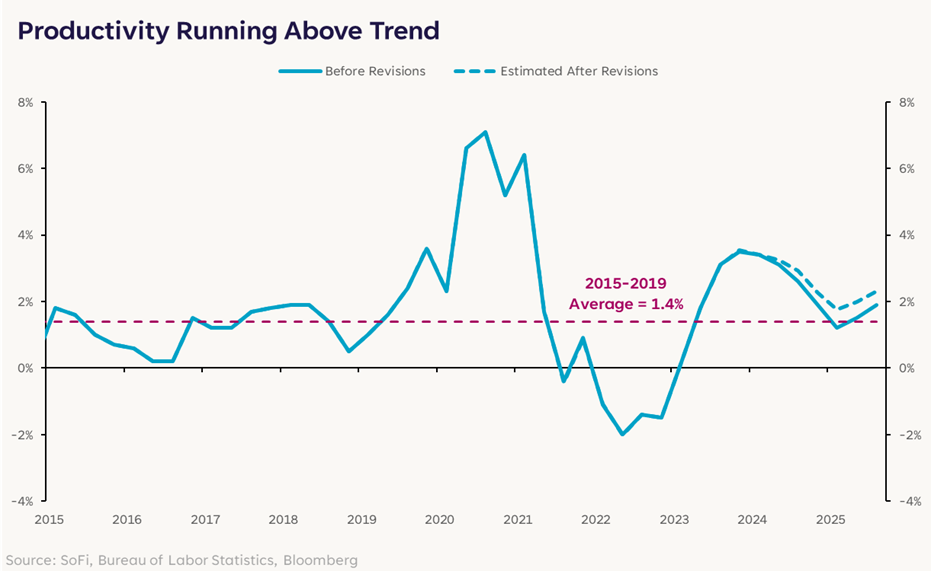

Productivity

Productivity is one of the most important elements in today’s economy. Simply put, this is a measure of how much output (GDP) we produce with a given amount of labor. And in the age of AI innovation, one of the main ways to measure its impact is to watch for gains that can keep GDP growth strong but not stoke inflation.

It’s difficult to measure the productivity gains that are directly attributable to AI. But we can observe improvements that line up with the timing of when AI started to infiltrate businesses and economic activity.

Productivity readings have been mostly above trend since mid-2023, with recent data showing a slight uptick in productivity after the brief hiccup around ”Liberation Day” in Spring 2025). And because employment data was revised lower, productivity figures are likely to be revised even higher. That’s a positive sign for economic growth and stability.

There are obviously risks to doing more with less, particularly if there are fewer jobs because they’re being displaced by AI. But that’s a topic that’s beyond the scope of this piece. Focusing on the near-term economic data, things appear to be supported by the increase in productivity.

Again… things appear to be fine, but not great. The U.S. has experienced three straight years of incredible stock market returns and strong economic data. We’ve watched inflation come down, wages go up, growth remain strong, and corporate earnings continue to surprise to the upside. It’s been a good run.

As cycles mature, those atypical data points start to become more typical, or muted. We believe that’s what we’re experiencing now. Unfortunately, we’ve seen a cooling in some economic data at the same time as considerable volatility in riskier parts of the market. That’s driving fears higher.

We would urge investors to continue focusing on sector and regional diversification. As the economy works through its new normal, a rotation to more value-oriented sectors and regions such as emerging markets is prudent this year. I don’t hear alarm bells, but there are some warning bells that reinforce a broader approach in 2026.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.