Decoding Markets: The Fed’s May Statement

Estimated reading time: 6 minutes

No Preemptive Moves

By looking at the Federal Reserve’s May meeting statement, you’d think not much had happened since the prior meeting.

The statement noted that economic activity expanded at a solid pace, the unemployment rate had stabilized at a low level, and inflation remained somewhat elevated.

With no official update to the central bank’s official economic projections, arguably the most important update in the statement was the declaration that uncertainty on the outlook had increased further, and the risks of higher unemployment and higher inflation (aka stagflation) have risen.

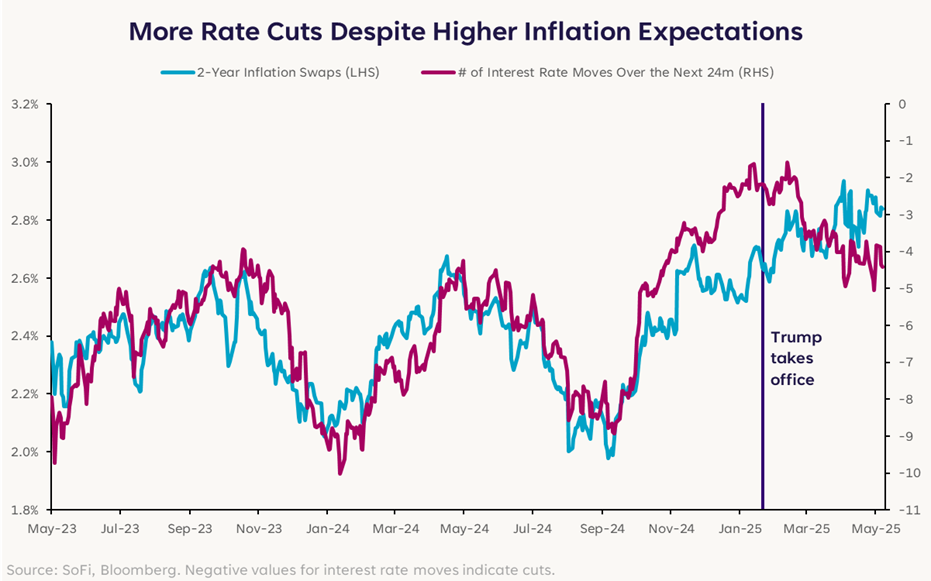

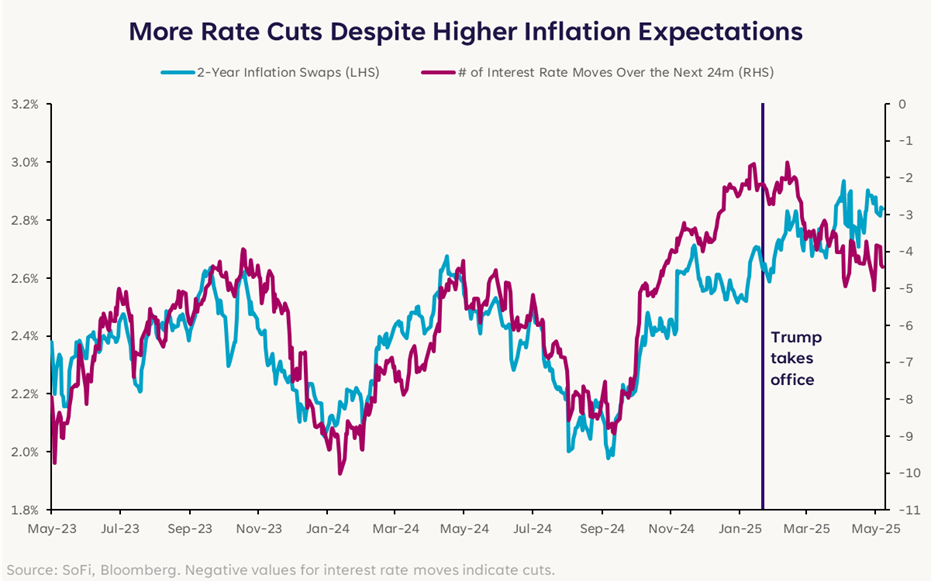

For now, it appears investors think labor market and growth concerns will take precedence over inflation. Over the next two years, investors expect headline CPI to average 2.84% and the central bank to lower interest rates by 1.10 percentage points (or four interest rate cuts with a 40% chance of a fifth).

Compare that to the beginning of the year when 2-year inflation expectations were 2.53% and 2-year rate cut expectations were 0.62 percentage points.

Under normal circumstances, such a trend might prompt the Fed to consider easing monetary policy to support growth, like it did in 2018-19. However, inflation was below the Fed’s target then – the same cannot be said now.

Chair Jerome Powell explicitly mentioned that they wouldn’t be able to preemptively act to support the economy this time, since cutting rates could exacerbate tariff-induced inflation and unanchor inflation expectations.

The wait-and-see approach signals a higher bar for policy easing, despite what some investors might be hoping for. Until the central bank gets the greater clarity it’s seeking, it seems the likeliest future moves it will make are no moves at all.

Global Trade Bellwether

In this unfamiliar new world we find ourselves in, the Fed takes a backseat. In its place, econ data and the resilience of global trade take center stage.

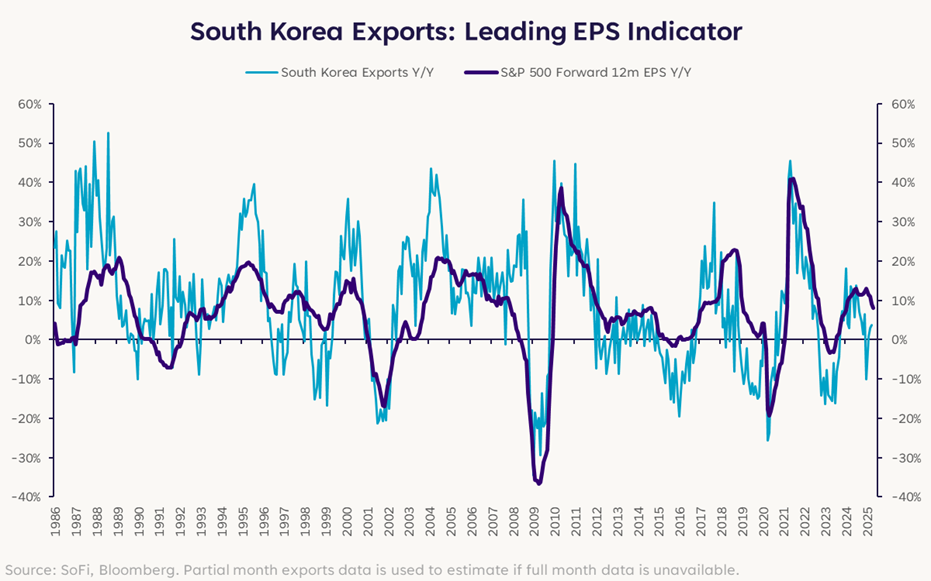

South Korea, with its export-driven economy and significant role in global supply chains, is a key indicator. The country’s status as a global economic bellwether stems from its position as a major exporter. It’s deeply integrated into global value chains, particularly in critical areas such as semiconductors, consumer electronics, and automobiles.

South Korean exports unexpectedly grew by 3.7% year-over-year in April, driven by a surprise surge in imports later in the month. This marked the third consecutive month of expansion, though below what was seen last year.

A significant driver of this growth was a surge in semiconductor exports, an acceleration from an already strong March. Notably this occurred alongside a decline in exports to the United States, while exports to other Asian neighbors and the European Union saw increases. The shift away from the U.S. could be a potential early sign of global trade rebalancing toward the Eastern hemisphere.

Implications for corporate earnings are mixed. While first quarter results have been generally solid, EPS guidance momentum is at its most negative in a decade, according to Bloomberg, with trade policy uncertainty throwing a wrench in what was supposed to be a banner year for businesses.

These dynamics underscore just how interconnected the global economy is. U.S. tariff policy has a direct and measurable impact on key trading partners like South Korea. The economic health of these export-oriented nations, in turn, influences global demand, which then affects the earnings of U.S. multinational corporations. The Fed statement speaks to this as well, noting that its assessments will take into account international developments.

Fleeting Volatility

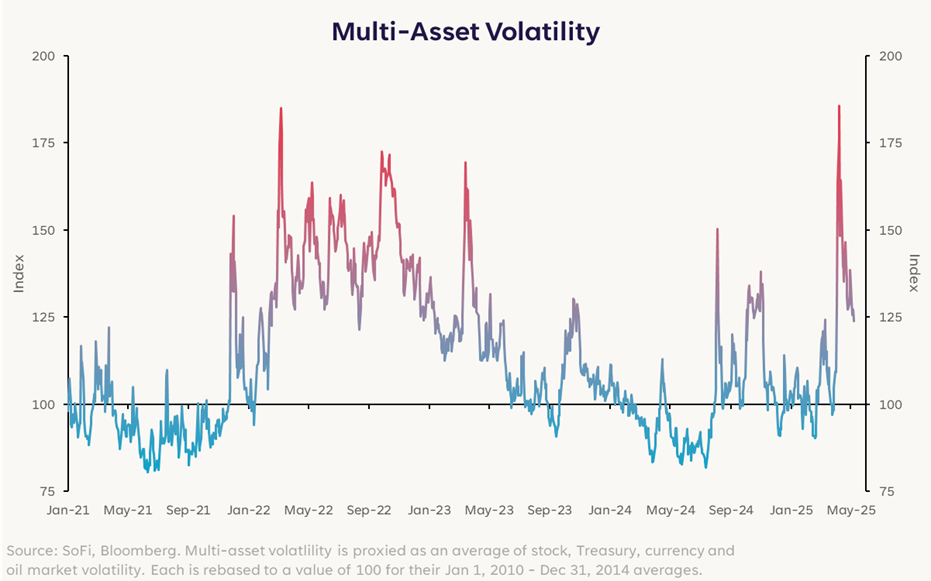

The impact of trade policy uncertainty can be felt across asset classes, with broad volatility spiking in early April to its highest levels since the onset of Covid. However, volatility has retreated relatively quickly since then, despite the ongoing uncertainty.

Even though the multi-asset volatility measure in the above chart has declined from its recent peak of 185 to 124 as of May 7, it remains above typical historical levels. A decline from “very high” to “high” is still high.

The market is somewhat aligned with the Fed’s cautious tone, though it looks like there’s more optimism priced in. This reflects, at least partially, a degree of hope for the future overriding the available facts on trade policy, particularly regarding tariffs on China.

Just how this will all play out remains up in the air, but every day that passes without a resolution on trade inflicts damage on the U.S. economy. In the meantime, investor sentiment will probably be reactive to news flow concerning these negotiations, with both successes and failures liable to reignite market volatility.

The relatively recent calm might be more fragile than it appears, and the Fed might not step in to save the day.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.