Decoding Markets: Round Two

Estimated reading time: 7 minutes

It’s a TACO Summer

Trade policy is back in the news again. In a move that echoes the Liberation Day announcement, the Trump administration has begun sending out formal letters to countries outlining the “reciprocal” tariff rate they can expect to pay starting August 1.

Unlike the first go around, however, the latest trade news has been met with little more than a collective shrug from investors. The S&P 500 is down less than 1% from its all-time high (which it recently set), while the VIX is at its lowest level since mid-February.

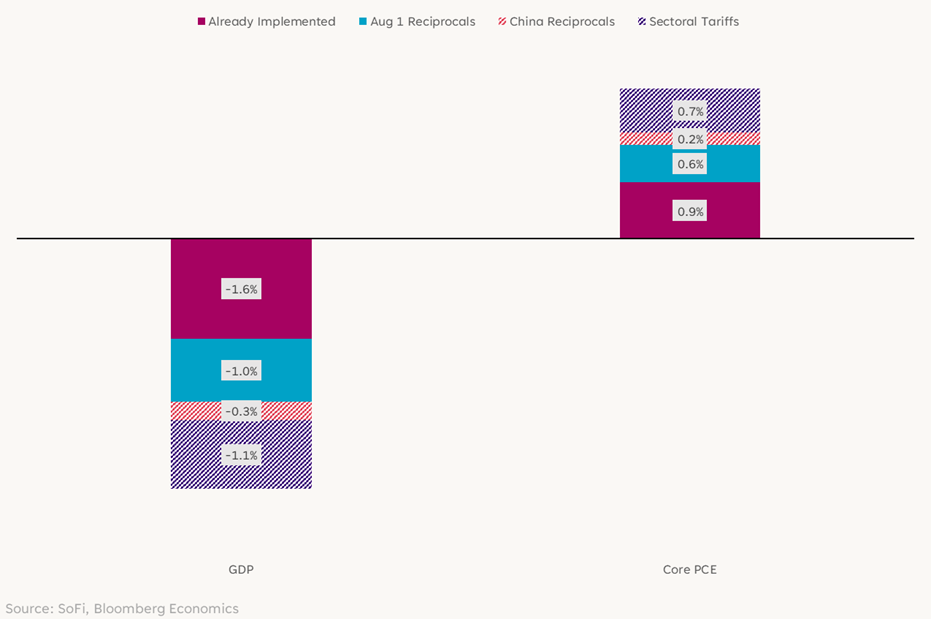

It’s unclear how much of the potential economic impact from tariffs has been priced in, but it’s hard to argue that the risks have fully been internalized. Bloomberg Economics estimates that the 2025 tariffs would reduce GDP by 2.9% and raise core PCE prices by 1.7%. Including the sectoral tariffs on strategically important goods such as semiconductors, copper, and pharmaceuticals that are planned in the future, the GDP and core PCE estimates intensify to 3.7% and 2.2%, respectively.

Estimated Impact of 2025 Tariffs

Yet calm prevails. The dominant explanation for the market tranquility — or complacency depending on who you ask — is the widespread belief in “TACO”, which stands for “Trump Always Chickens Out.” In a nutshell, it’s the idea that the administration has a very low tolerance for significant economic pain and will back down from its most aggressive threats when faced with a sharp negative market reaction.

The belief isn’t without precedent. The first 90-day delay on tariff implementation came after stocks began falling into bear market territory and Treasury yields surged. This pattern of threat, market tantrum, and policy retreat has been repeated in dealings with China and the European Union, reinforcing investor belief that when push comes to shove, de-escalation will inevitably be the default outcome.

The TACO concept poses some risks, however, as it has contributed to a market environment “priced for perfection”. Investors expect that an economically damaging trade war will be averted, which creates a highly asymmetric risk profile. The best-case scenario – a negotiated de-escalation – is already priced in, which limits the potential market upside from a positive trade resolution, while the downside is largely written off. Thus, a paradox emerges. TACO depends on the administration responding to severe market pressure, but because investors are so confident it will happen, they’re not selling. The absence of a negative market reaction removes the feedback loop that makes TACO work. This could inadvertently enable the very outcome investors are betting against, as the administration may feel less pressure to de-escalate without a market panic to react to.

Dollar Doldrums

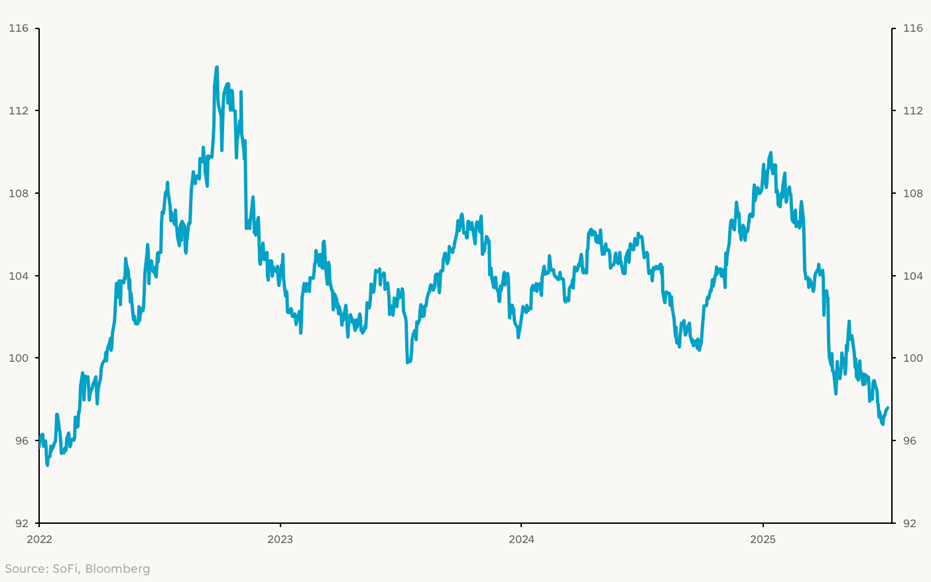

Complicating the tariff calculus is the dramatic shift in the value of the U.S. dollar. Unlike previous trade disputes where a strong dollar acted as a buffer, the dollar has actually been in a steep decline.

In the first six months of 2025, the index plunged 10.7%, marking its worst first-half performance since 1973. The DXY is trading below the 98 level, near its lows of the last three years. The weakness is being driven by a confluence of factors, including unpredictable U.S. policy and growing fiscal deficits, which are prompting foreign investors to reduce their holdings of dollar-denominated assets.

Importantly, this is the inverse of what happened during the 2018 trade upheaval. At that time, the dollar strengthened after tariffs were announced, which provided a buffer against the inflationary impact of tariffs. A weaker dollar on its own is inflationary because it takes more dollars to purchase the same amount of foreign goods. But when combined with tariffs, the inflationary impact is amplified and creates a double whammy for consumers and businesses.

This puts the Federal Reserve in a tough spot. On one hand, the clear upward pressure on prices would normally dictate a hawkish policy response. On the other hand, the tariffs are widely expected to act as a drag on economic growth and employment, which would normally call for lowering interest rate cuts to support the economy. The tensions between the Fed’s goals makes the future path of monetary policy uncertain.

U.S. Dollar Index

Earnings Showdown

For the large multinational corporations that dominate the S&P 500, the weak U.S. dollar is actually a positive. There are two primary benefits. First, a weaker dollar makes U.S. exports cheaper and more competitive for foreign buyers, which can help stimulate demand and drive top-line revenue growth.

Second, it creates a positive translation effect on earnings. Any revenue and profit generated in foreign currencies are converted into dollars for reporting purposes, and because the dollar has weakened, that conversion results in a higher dollar value.

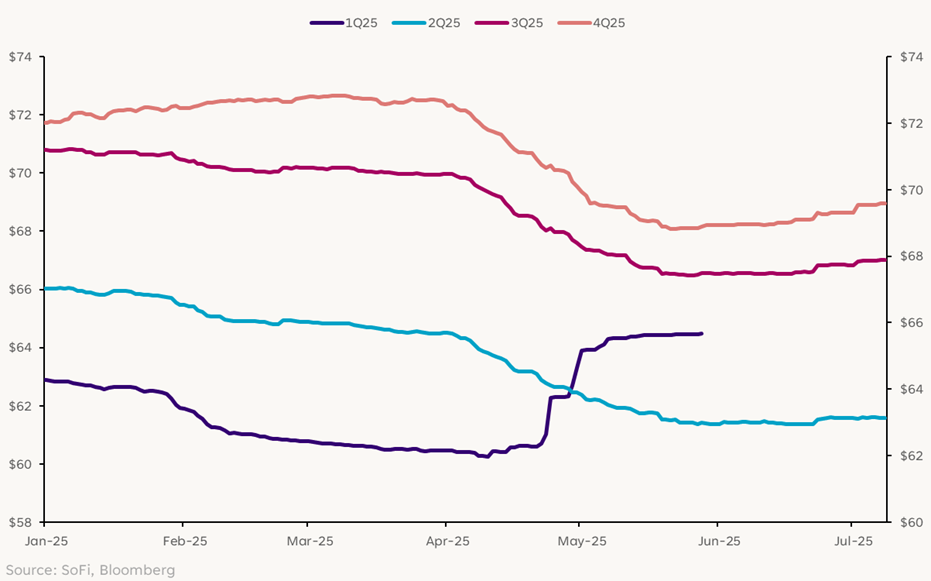

That brings us to the second quarter earnings season, where the dominant narrative is one of a lowered bar. Consensus earnings estimates fell for most of the quarter, with Q2 EPS for the S&P 500 index now expected to increase by just 4.1% year-over-year after beginning April at 8.4%. It wouldn’t be much of a surprise if companies are able to beat expectations, considering how much estimates have come down. Still, that might not be enough to secure positive price reactions. Given how fast the economic landscape is shifting, the main focus this earnings season probably won’t be the backward-looking Q2 results, but the forward-looking guidance that companies provide. In this regard, consensus expects EPS to ramp up in the second half of 2025, with this expected pickup in profitability a crucial pillar supporting the market’s current valuation. Beats on earnings will get overshadowed quickly if a company’s outlook for the third quarter and beyond is cautious or fails to validate the optimism baked into its stock price.

S&P 500 EPS Consensus

With markets priced for perfection, a lot is riding on the upcoming earnings season and what companies tell us about the outlook. Any failure to confirm the lofty expectations for an earnings acceleration in the second half of the year could serve as the catalyst that shatters the TACO-fueled calm. While this doesn’t necessarily mean a return to the frenetic swings we saw in April, a period of heightened market choppiness could be on the horizon.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.