Decoding Markets: Growth Scare

Estimated reading time: 6 minutes

Will the Real Economy Please Stand Up?

Investing is never free of uncertainty, and that has felt especially true in the current macro environment. With the release of the first quarter GDP report, however, clarity is dipping its toes back into the market ever so slightly. Let’s dive in.

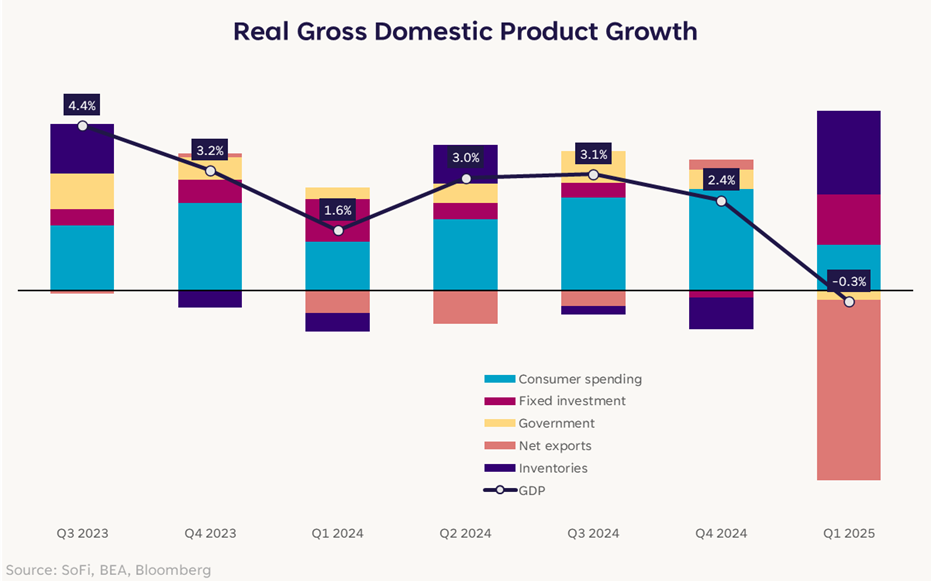

Economic growth in Q1 2025 showed a much anticipated deceleration, with real GDP contracting an annualized 0.3%. This marks the first contraction since Q1 2022 and a significant slowdown from the 2.4% growth figure last quarter. While typically alarming, this headline figure warrants a closer look, as it was heavily influenced by volatile components rather than a fundamental collapse in economic activity.

The negative Q1 reading was primarily driven by a massive surge in imports and significant changes in business inventories. Imports spiked a dramatic 41.3%, causing the Net Exports component to drag down growth by 4.8 percentage points. Simultaneously, businesses increased their inventories, adding back about 2.3 percentage points to growth, but not enough to offset the import drag.

This unusual activity was a direct consequence of businesses responding to trade policy upheaval. Evidence suggests that companies — particularly those reliant on foreign goods like transportation equipment, pharmaceuticals, and computers — rushed orders to bring them into the country before potential tariffs made them more expensive. This led to both the recorded import surge and the related build-up in inventories as companies stockpiled goods.

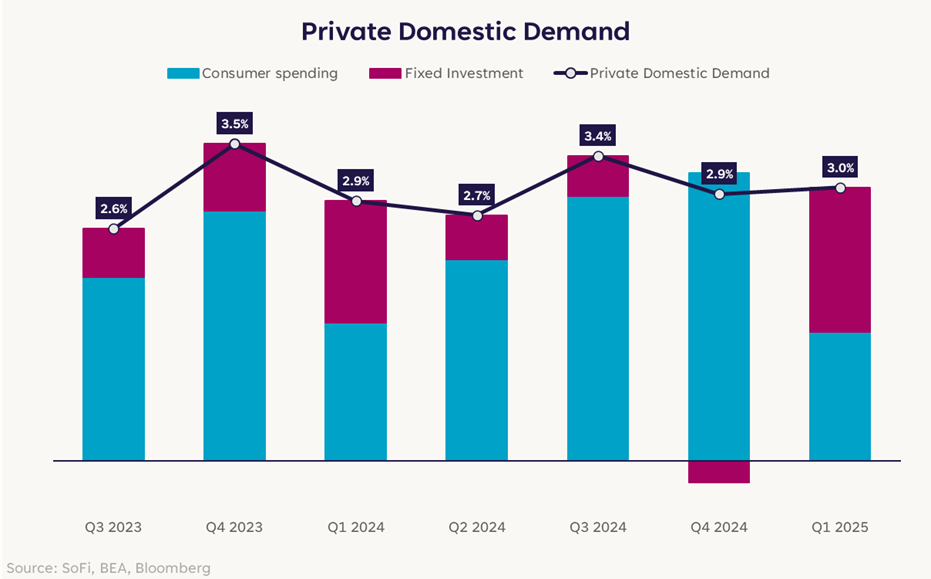

To gauge underlying economic momentum, economists often look at “real final sales to private domestic purchasers,” more casually known as private domestic demand. This measure excludes government spending and volatile trade and inventory effects, which can be helpful when the broader data is being possibly distorted. In stark contrast to the headline GDP figure, this measure grew a solid 3.0% in Q1. Consumer spending did slow a bit, but private fixed investment picked up the slack.

Bond Market Puzzle

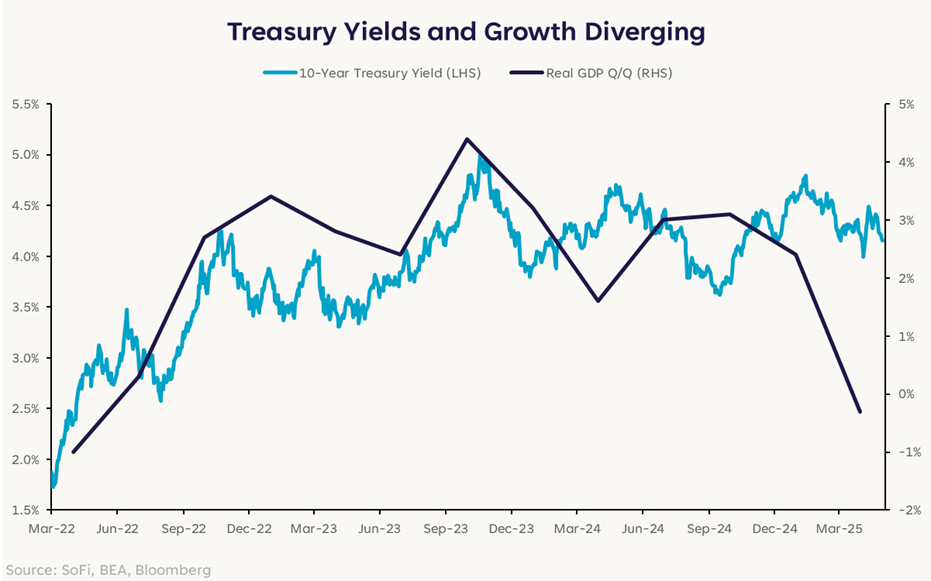

Historically, Treasury yields tend to rise when the economy is expected to grow strongly and fall when it’s expected to slow or contract. This relationship exists because strong growth can fuel higher inflation expectations and potential interest rate hikes by the Federal Reserve.

That dynamic held in recent years, but the latest GDP print brings it into question. Despite the weak -0.3% headline GDP in Q1 and recession fears, the 10-year Treasury yield is still around where it began the month at 4.15%-4.20%.

There are lots of possible reasons for this disconnect. For instance, some investors posit that inflation fears associated with tariffs could be boosting yields. After all, core PCE inflation accelerated from 2.6% to 3.5% in Q1, but this theory doesn’t seem exactly right. Looking at the difference in yields between nominal Treasurys versus Treasury Inflation-Protected Securities (TIPS), we can see that 10-year inflation expectations have actually fallen from 2.37% to 2.23% since the start of April.

Instead, an “all of the above” explanation is probably needed to explain the stickiness of higher yields. Investors could be looking past the distorted GDP figure in part, and focusing on some of the worrisome inflation data and the relatively resilient underlying domestic demand data. Additionally, heightened uncertainty around trade policy and the Fed’s future actions, as well as waning foreign investor appetite for investments in the U.S. may be pushing up the “term premium” – extra compensation investors demand for holding longer-term bonds amid increased risk.

Staring Into the Unknown

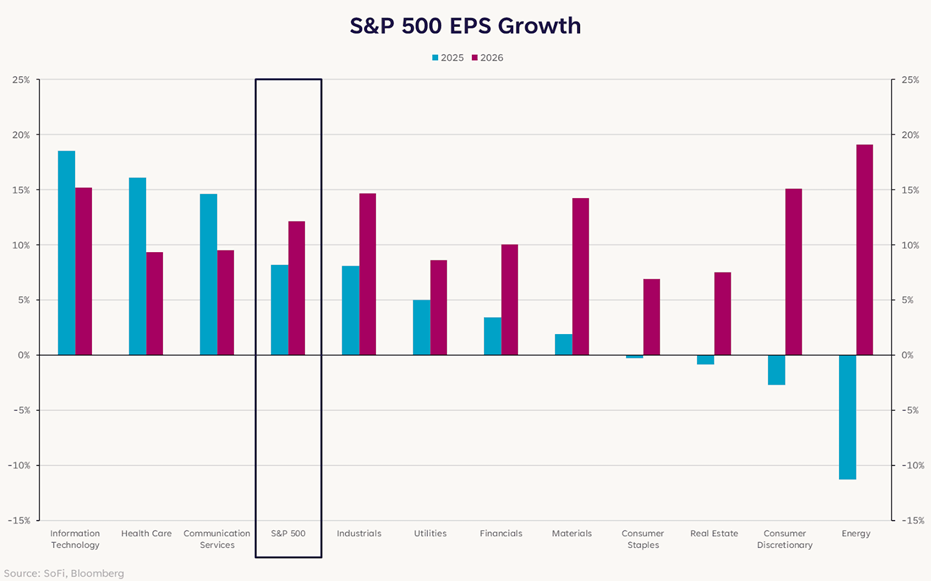

The combination of slowing headline growth (-0.3% Q1 GDP) and persistent inflation (+3.5% Q1 Core PCE) has revived concerns about stagflation – a period of stagnant economic activity coupled with high inflation. How this will all impact corporate earnings is unknown. S&P 500 companies have beat consensus expectations by more than 9% so far this earnings season, yet the rapidly shifting landscape means that in many ways, the results are already stale.

Companies exposed to imports have been hesitant to give much guidance on future quarters, while analysts on the whole have not revised earnings much in the grand scheme of things. Indeed, consensus currently expects solid earnings growth this year and next.

Sectors more sensitive to trade policy uncertainty are expected to have weaker earnings than other parts of the market, but given resilient current expectations, there’s room for these numbers to change in the coming months. A recession would almost certainly weigh on earnings, but an inflation acceleration complicates the picture since price increases could boost nominal earnings even if real growth is challenged. That’s similar to what happened from 1980-1982: From the start of the 1980 recession through the end of the 1981-82 recession, trailing 12-month earnings fell just 3%. The same can’t be said for stock prices, however, as those periods saw drawdowns of 17% and 27% despite the resilient earnings.

Much will depend on how trade policy plays out and how businesses and consumers respond, but for now the market remains on a razor’s edge.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.