Decoding Markets: April Inflation

Estimated reading time: 7 minutes

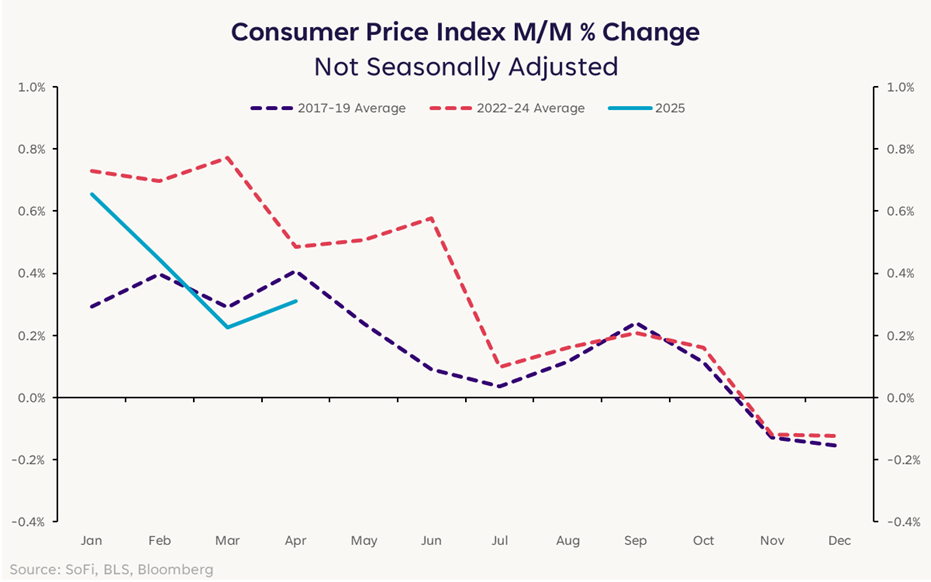

Gentle Dip

April’s inflation data offered a welcome downside surprise, with the Consumer Price Index rising less than investors had expected in April: 0.2% instead of 0.3%. That puts the year-over-year rate at 2.3%, the lowest since February 2021, when the economy was just beginning to grapple with the initial wave of pandemic-related price surges.

Drivers of the cooler rate were mixed. Housing costs remain a primary contributor, while increases in natural gas and electricity costs also added to the overall inflation rate. On the other hand, food prices declined 0.1% (the first overall decline since July 2020), with egg prices plunging a whopping 12.7%.

All in all, recent data suggests a disinflationary trend through April. This is especially evident if you look at the seasonally unadjusted data. After a brief spike at the start of the year, actual price increases have been below what we’ve seen in recent years and in-line with pre-pandemic levels.

For investors, a return to a more predictable and lower inflation environment would typically imply lower interest rates and calmer market conditions — and potentially higher P/E multiples as a result. But tariffs could still disrupt the optimistic disinflationary trends in the data. While the recent detente between the U.S. and China has boosted investor sentiment, trade policy uncertainty lingers.

That uncertainty can act as a significant drag on economic activity. Businesses faced with unpredictability regarding future input costs, supply chain stability, or access to international markets may slow their capital expenditure and hiring plans. That, in turn, can dampen overall economic growth.

The Fed’s Next Move

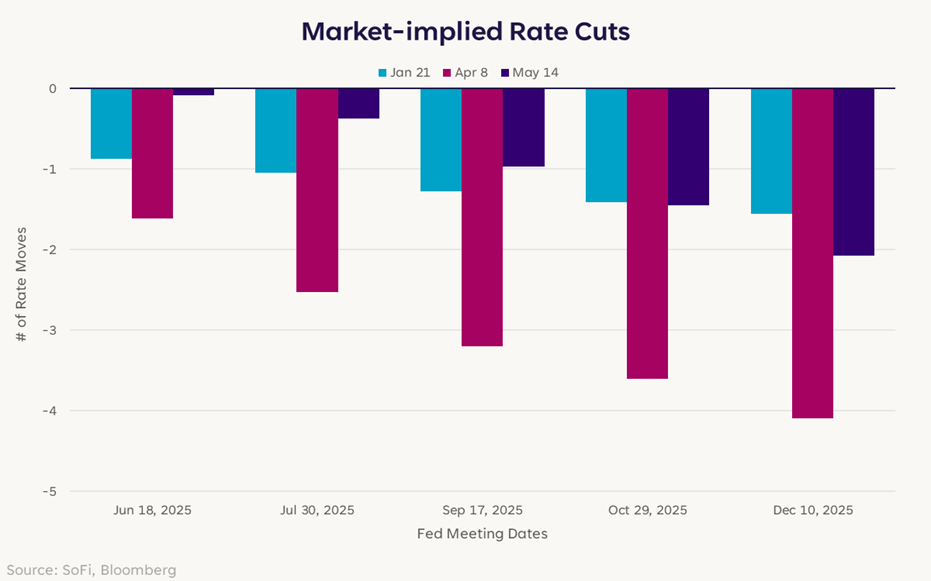

At the beginning of Trump’s second term, market pricing pointed towards one or two interest rate cuts by the Federal Reserve in 2025.

As trade upheaval intensified in March and April, however, recession fears rose. Investors began to anticipate that the Fed would act to support the economy, despite the risk of inflation shocks. Since then, expectations for cuts have eased with year-end expectations now near where they were before all the turmoil.

Nevertheless, tariffs remain a major wildcard in the Fed’s policy deliberations. As things currently stand, they’re paused, not fully ruled out. And because the tariffs pull at the Fed’s dual mandate of price stability and maximum employment, that could lead to higher inflation and higher unemployment.

That leaves the Fed caught between a rock and a hard place – lower interest rates to protect the labor market and inflation may spiral higher, keep rates high to fight inflation and the economy could weaken significantly. The ongoing disinflationary process could be disrupted down the road if additional tariffs take effect.

If that weren’t enough, the Fed’s emphasis on being data-dependent means that it is unlikely to act if the economy’s trajectory is unclear. And without a resolution on the trade front, it’s hard to get clarity. This all suggests that the Fed could adopt a more cautious “wait-and-see” approach. Current market pricing indicates a 97% chance of a rate cut by September, but the 90-day pauses on tariff implementation means that could move around a bit.

Shape of the Curve

Trade policy has been the main focus of investors over the last few months. That is likely to continue, but interest rate policy is a contender for second place. In what is sure to be a volatile period for interest rates, focusing on the Treasury yield curve could offer valuable insights for investors – even for those that invest primarily in stocks.

The last week or two has mostly consisted of what is called bear flattening, an environment where Treasury yields rise, with shorter-term yields rising more quickly than longer-term maturities. This dynamic emerged as the market priced out the possibility of interest rate cuts. Such environments often correspond with mixed, but generally positive, stock market returns, as we’ve seen this month.

But forward returns depend on how the future evolves. If we had a crystal ball and knew what the yield curve would do, it would be easier to invest. Alas, we don’t, but that doesn’t mean we can’t come up with some ideas.

If the economy remains resilient and tariff fears ease further, we could see bear flattening continue as rate cuts get priced out further. Maybe instead of two rate cuts this year, the Fed doesn’t cut at all. Sector performance during bear flattening phases tends to be quite varied, without a single, consistently dominant theme.

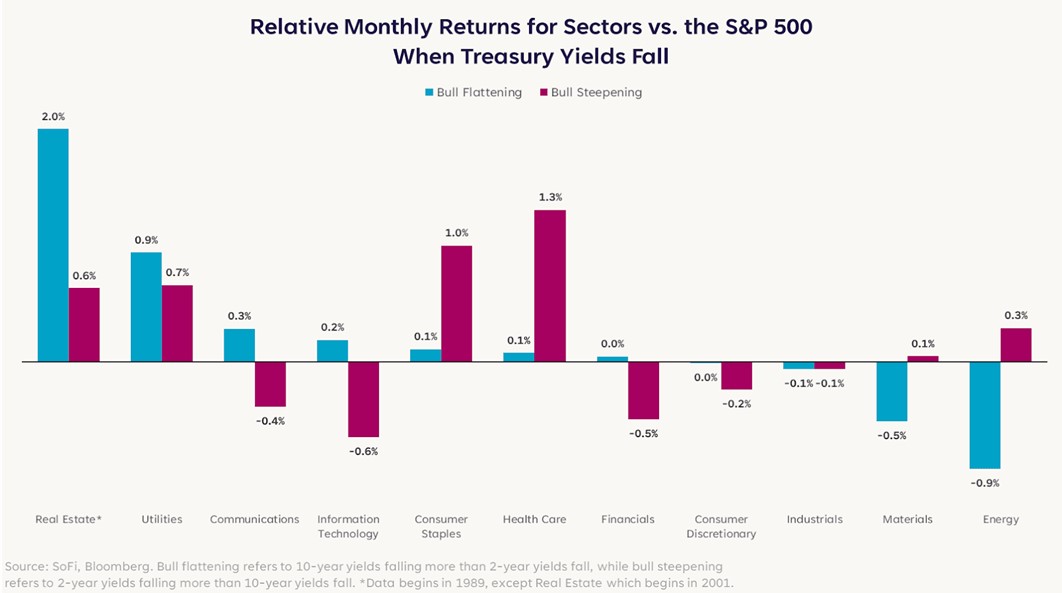

On the other hand, if the economy weakens we could see Treasury yields fall (in other words, a “bull” move for bonds). When Treasury yields are falling (a “bull” market for bonds), the implications for stocks depend significantly on how the yield curve’s shape changes. The two main possibilities here are bull flattening and bull steepening.

Scenario 1: Bull Flattening (Long-term yields fall faster than short-term yields)

- This move is often driven by expectations of lower long-term inflation, a flight to the safety of longer-dated bonds amid economic uncertainty, or expectations that slower economic growth in the future will allow the Fed to eventually lower interest rates.

- This environment is usually pretty positive for stocks and typically occurs more often during late-cycle environments. It has historically favored sectors that are more sensitive to changes in long-term interest rates like Real Estate, Utilities, and Technology.

Scenario 2: Bull Steepening (Short-term yields fall faster than long-term yields)

- This move typically happens when the market expects the Fed to lower interest rate cuts in order to stimulate an economy that is either weakening or is in recession.

- While interest rate cuts are usually beneficial for stocks, the economic conditions that need to be present for the Fed to lower interest rates meaningfully are usually negative for stocks. Defensive sectors such as Utilities, Consumer Staples, Health Care, and Real Estate have historically outperformed the broader market in these environments.

Bull flattening periods usually come before bull steepenings – an economy usually decelerates before it falls into recession – but it can be hard to pinpoint the transition point. Investors may cheer for lower interest rates, but any potential gains can quickly reverse if a significant economic slump gets priced in.

In those moments, a more defensive portfolio posture would help partially insulate against stock market declines. That might be worth considering given lingering trade uncertainty, but as the saying goes: There’s no such thing as a free lunch. A favorable resolution on the trade front with no major economic slowing could boost cyclicals.

Investing isn’t always easy, but it’s worth it in the long run. Stay diversified and stick with it.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.