Looking at: The Fed’s December Meeting

Estimated reading time: 0 minutes

What a Buy

Typically, we’d start a Fed column by discussing the rate move. This time, we’re going to start with what we believe is the more important part of today’s announcement.

Starting on Dec. 12, the Federal Open Market Committee will start buying Treasury bills again at a rate of $40 billion/month. This will last until April, when the rate of purchases will possibly come down to $20-$25 billion, according to Chair Jerome Powell.

Since this newest round of Treasury buying is coming only 11 days after the latest quantitative tightening (QT) effort ended, the message seems to be that the Fed tightened too far and needs to reverse course in order to support market liquidity.

That’s not to say that there is an obvious or broad reaching liquidity problem affecting stocks. At this point, there is not. But overnight funding markets (banks borrowing from each other and banks borrowing from the Fed) have shown recent signs of funding stress that likely led to this about-face.

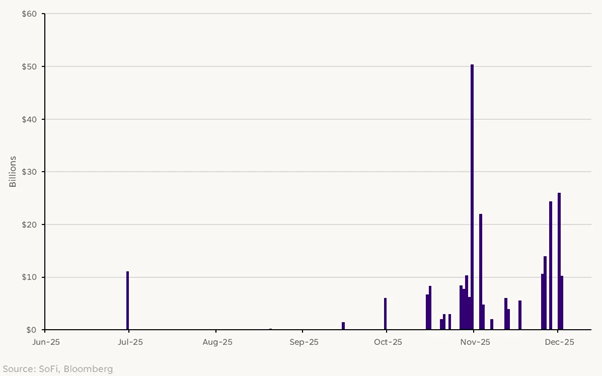

For example, greater usage of the Fed’s standing repurchase facility — a backstop that allows banks in good standing to exchange Treasurys for cash overnight — suggests more banks are short on cash.

Standing Repo Facility Usage

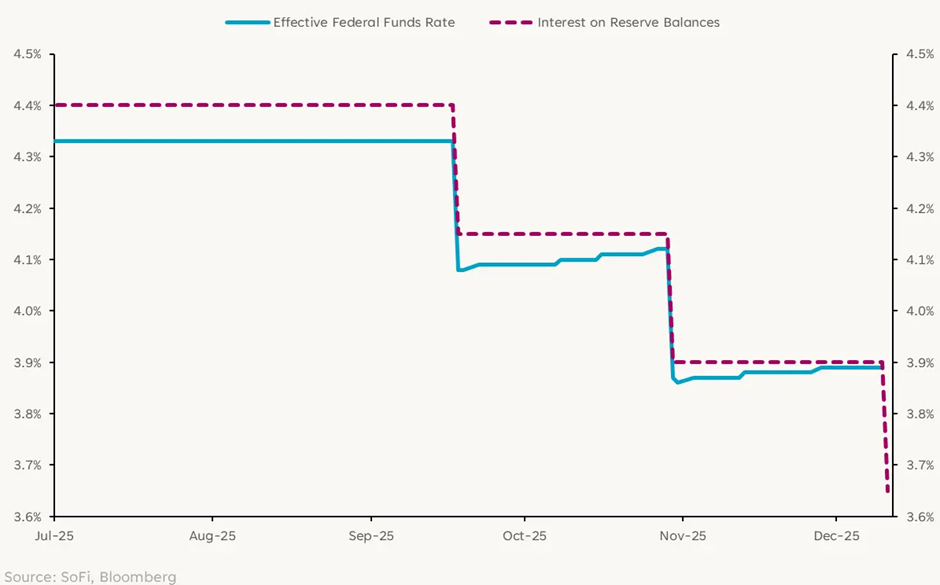

Another force at play is the level of bank reserves. We spent most of the past three years in “abundant reserve” territory, but now we’re down to “ample reserve” territory, thanks to QT and a reverse repo facility that could no longer absorb it.

Although ample is where the Fed wants reserves to be, we believe they actually started to flirt with “scarce,” which required the Fed to act. Though there’s no specific threshold, the Fed starts to take notice as the spread between interest on reserve balances (dashed magenta) and the effective funds rate (blue) narrows.

Benchmark Interest Rates

Powell downplayed this T-bill purchasing announcement by explaining that:

• engaging in some Treasury buying was the plan all along,

• expanding the balance sheet regularly is necessary to support bank reserve balances, and

• the Fed is trying to get ahead of April 15, when reserve balances drop temporarily because of taxes being paid.

The Fed is calling this move “reserve management purchases” to signal that this is not intended as a form of quantitative easing (QE).

Is That Good or Bad?

It’s complicated. The market liked it, the 2-year Treasury yield fell 10 basis points, and the S&P 500 finished in the green, with economically sensitive sectors such as Industrials, Materials, and Consumer Discretionary performing the best.

In the near-to-medium term, I think the message is bullish for stocks and short-term Treasury bonds. We also take this as an indication that the Fed is ready to engage in classic QE if it should become necessary. Given markets’ dependence on Fed driven liquidity, this is likely to be seen as a friendly move for risk assets.

However, it also runs the risk of stoking inflation and feeding more speculative behaviour in markets. The effect is likely to be multifaceted.

Looking Ahead

A new Fed Chair will take office in May, and as of now we can only expect Powell’s replacement to be dovish on rates, which would align with the administration’s well-published wishes.

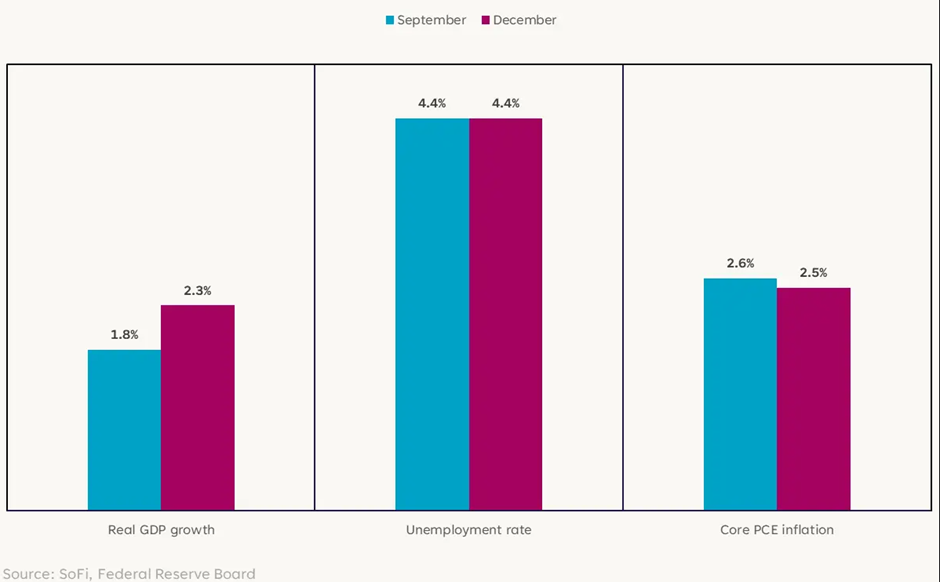

Outside of rate expectations, the Fed gives us a summary of their projections once per quarter. Today’s meeting included an update to those projections, and the tone was quite positive. Compared to its statement in September, the Fed expects 2026 growth to be stronger, inflation to be cooler, and unemployment to remain steady.

Fed Summary of Economic Projections for 2026

Given this picture, and the expectation for further (though not imminent) rate cuts, it’s difficult to be negative on the market or the economy. Despite the Fed acknowledging concerns about the labor market, officials seem confident that weakness can be stymied by supportive policy and a stable growth environment.

The consensus view right now is widely held across investors: There’s general positivity that growth will reaccelerate in 2026, the consumer will keep spending, inflation will stay contained, and markets have potential to produce attractive results, once again.

Sometimes, everyone thinking the same thing is a warning sign. But other times, the consensus view is right.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.