The Fed’s June Statement

Estimated reading time: 0 minutes

Cuts, Party of One

Not only did we have a Fed statement today, but an inflation report as well. That’s what We’d call a humdinger of a day, especially in this cycle when inflation and Fed moves have been some of the strongest drivers of markets, both up and down.

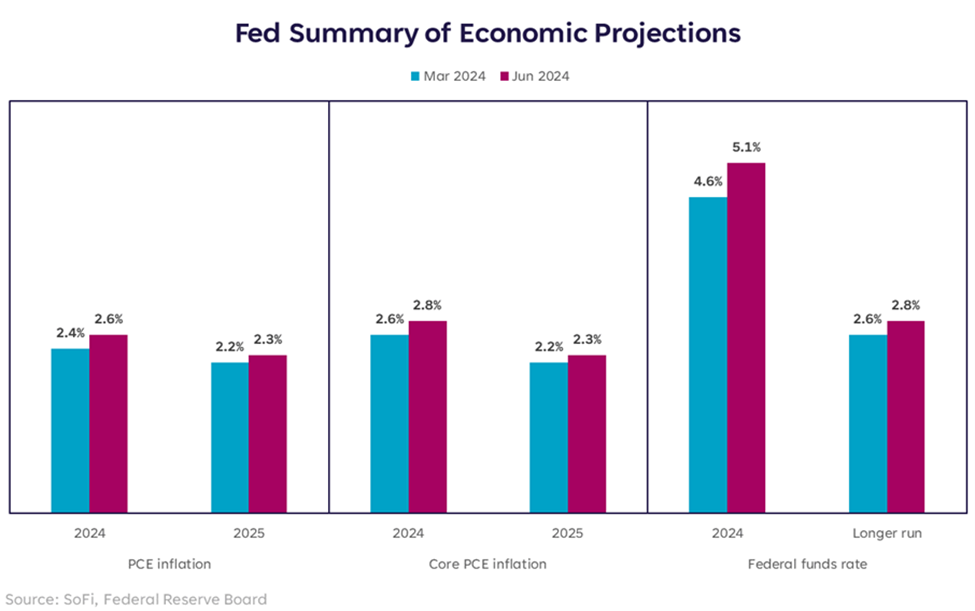

However, despite cooler-than-expected CPI data released earlier in the day, the Federal Open Market Committee’s (FOMC) updated summary of economic projections (SEP) and a dot plot showed a higher year-end inflation rate and fed funds rate than it did in March.

In other words, the median dot now suggests only one cut in 2024, down from three cuts expected at the March meeting. In addition, the longer-run fed funds rate expectation moved up, which suggests that higher for longer just went… higher.

Chair Powell’s commentary remained measured, reiterating the FOMC’s commitment to getting inflation on a sustainable path toward 2%. He also acknowledged the progress that has been made, but indicated that the base effects (the comparisons to data from one year prior) could make progress on inflation harder to see in the second half of this year. Basically, since inflation stopped rising as quickly from June to December of 2023, it’s not going to look like it’s falling very quickly when compared to the same periods of 2024.

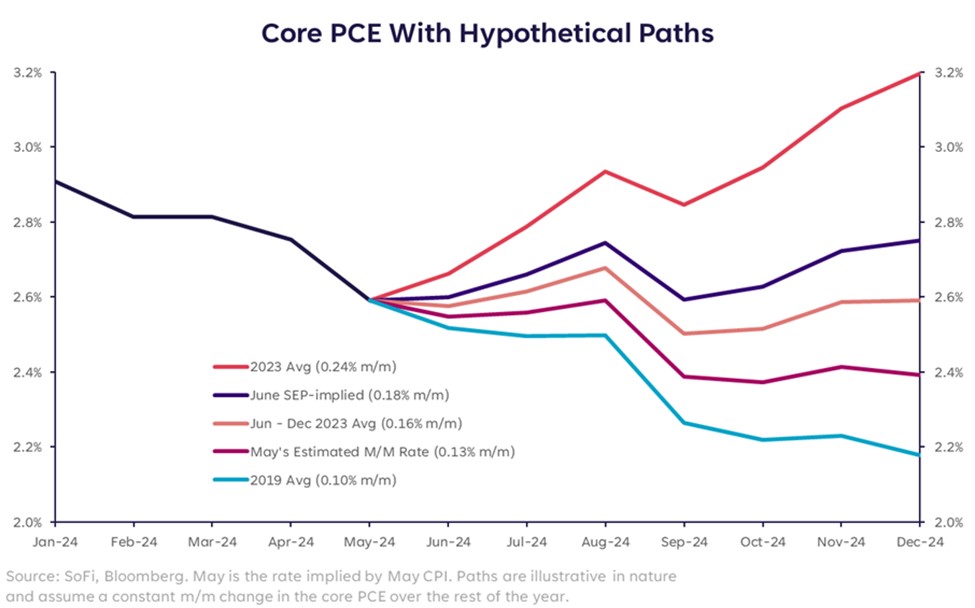

The below chart shows a number of possible scenarios. Each path assumes an average month-over-month rate for the remainder of the year. Obviously, inflation will not come in at the same level every month, so this is purely for illustrative purposes. What’s important to note about this chart is that the path most consistent with the Fed’s recent projection (dark purple) for Core PCE suggests a monthly run rate that’s higher than the latest print. That implied rate of growth is also above pre-pandemic levels and the levels we saw in the second half of 2023.

We could read this as the Fed suggesting that inflation is going to, again, get worse before it gets better. Despite that being an unwelcome message for consumers, the S&P 500 and Nasdaq chose to focus more on the fact that May inflation data came in cooler, and held on to a decent amount of their morning rallies. Treasury bonds gave back about half of their yield drop by the end of the day, but still finished the session sharply lower on increased expectations of a September rate cut.

On a Knife-Edge

All of these market moves could change tomorrow as there is always a digestion period post-CPI releases and post-FOMC statements.

Somehow, things became even less clear than before, and the Fed left its message in a gray area that didn’t bring us any additional clarity on how long this rate pause may last. Yet markets mostly celebrated the ambiguity. We think that’s partly because CPI mattered more than the FOMC today, and partly because the market is choosing to believe that even if inflation doesn’t cool further, the economy will stay strong enough to absorb it, and AI will take care of the rest.

We find it difficult to believe that: 1) the market will cheer if we make no further progress on inflation for the rest of the year, 2) other economic data will stay strong enough to help us see through that, and 3) that the Fed will perform its first rate cut two days after the U.S. election.

Stranger things have happened, and strange things happen all the time. But We’ll bet this narrative changes quite a bit in the next couple quarters.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.