Possible Paths

Estimated reading time: 5 minutes

Worth the Wait?

Here’s what we know: Rate cuts are starting later than we thought. Here’s what we don’t know: When they do begin, how quickly will they progress?

This got us thinking: What might markets look like in different scenarios? Right now, fed funds futures are pricing in a scenario where the Fed cuts rates slowly, methodically, and – because they want to not because they have to–a gradual and smooth normalization of policy.

But if history serves as any guide, hiking cycles tend to be more gradual and methodical, while cutting cycles tend to be more swift and dramatic. Although a “cut because they want to” strategy is undeniably more desirable for the economy and markets, there’s a good chance that might not be how it shakes out.

Cutting Fast and Slow

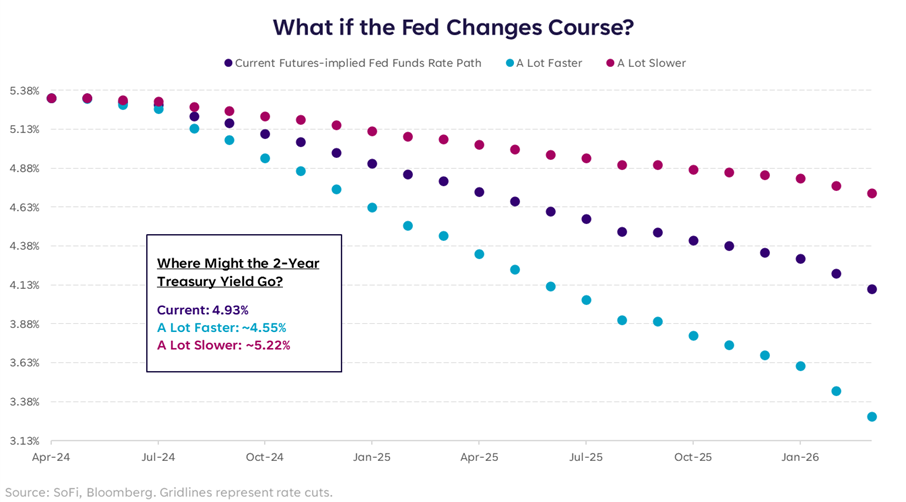

There’s no way of knowing how every variable would react to a cutting cycle that happens at different speeds, but for the purpose of this piece we focused on two very important variables: the 2-year Treasury yield and the U.S. dollar.

As cuts were pushed back further, the 2-year yield rose notably, from 4.14% on January 12 to 4.93% at time of writing. The 2-year yield is thought to closely track the fed funds rate, so it’s no surprise that it has seen a dramatic move while rates are expected to stay higher for longer.

But what the current 2-year yield doesn’t take into account is the possibility that the Fed will either have to cut sooner and faster than expected – likely in reaction to weak data or a shock – or that the Fed will push cuts back even further, and do them more slowly – likely if inflation stays elevated and the economy remains strong.

By our estimation – based on our own embedded assumptions of timing and magnitude, and for illustrative purposes only – the current 2-year yield would have to move if things changed.

There are good things and bad things about a move in the 2-year in either direction, but in the case of an even higher yield (later and slower cuts than currently expected), we think the bad starts to outweigh the good. For individual investors in money market funds, short-term Treasurys, or interest-bearing accounts, this is a good thing. For capital availability, the U.S. government’s borrowing costs, and the interest cost to banks, this is a bad thing.

Not to mention, the yield curve is likely to stay inverted. There’s no telling what would happen in the 10-year Treasury yield, but even if we assume a uniform rise, a move toward 5.2% in the 2-year would put 10-year yields at roughly 4.9%… The last time the 10-year yield was at 4.9% the S&P was 16% lower at 4,200.

Higher yields are likely to become untenable for investors – either because of the absolute level, or because of how long they’ve lasted.

Don’t Forget About the Dollar

We sit at an interesting juncture in the world where central banks are now moving in different directions. This is having a strong impact on currencies, particularly the dollar, which continues to strengthen against most foreign currencies.

In a very straightforward environment, a country’s currency strength or weakness follows its interest rates up or down, respectively. Given the recent rise in yields, it’s only natural that the dollar has strengthened too.

If rate cuts continue to be pushed back, and are expected to move even slower, the dollar is likely to continue its rise.

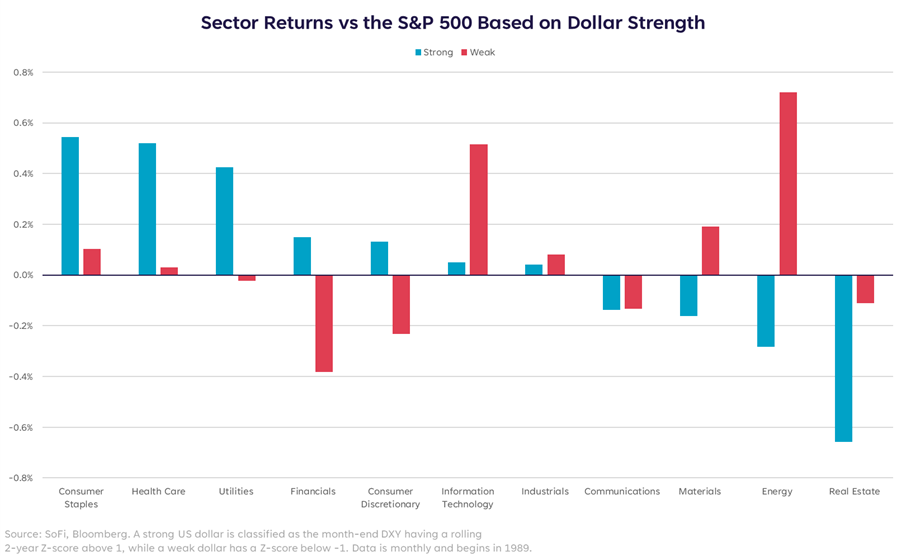

Given the current trend, looking at sector performance in an environment where the dollar strengthens further might be useful for portfolio positioning.

What’s surprising right now is that despite recent dollar strength, the current level doesn’t hit our threshold for a notably “strong dollar” environment… but we’re close. The current U.S. dollar spot rate is trading at roughly $106, it would move into “strong” at about $108.

A more interesting piece of this puzzle is that the sectors that outperform during strong dollar environments are defensives – staples, health care, and utilities. That’s because generally, the dollar is seen as a safe haven asset during times of global stress. So it’s not that simple to say a stronger currency is good, strength may not come for the reasons investors want it to.

This period is quickly turning into the next act of a movie about a global experiment in monetary policy. History has not served as the guide we hoped, which makes the future more murky. Markets seem to be feeling that lack of visibility, and global central banks are trying to protect their own financial systems against mounting currency and rate divergences.

We think we’ve moved back into an environment where anything could happen, and headline risk is high. Staying invested is still important, but we need to choose our assets wisely and measure our risk tolerances carefully given the circumstances.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.