November 2023 MARKET LOOKBACK

Estimated reading time: 5 minutes

Recent progress on fighting inflation continued in November, with consumer and producer price indexes decelerating further. The labor market cooled slightly, but remained generally resilient. The Federal Reserve held its policy rate steady at an upper bound of 5.50%, with multiple officials opining that monetary policy was at a sufficiently restrictive level to get inflation back to target. Treasury yields plunged on all of this data as expectations for rate cuts increased, and stocks and bonds had one of their best months in decades.

Macro

•Q3 GDP was revised up to an annualized, seasonally adjusted rate of 5.2% from 4.9%, while the first GDI estimate was released at 1.5%, continuing the ongoing divergence between the two measures of output.

•The Fed held the fed funds target rate at a range of 5.25%-5.50%, with multiple officials indicating their belief that monetary policy was at a sufficiently restrictive stance to bring inflation down to the 2% target.

•150k jobs were added in October, while the prior two months saw net revisions of -101k.

•October CPI and PPI surprised to the downside on both headline and core measures, and in both m/m and y/y timeframes.

•Homebuilder sentiment declined to an index value of 34, the lowest since December 2022 and well below the neutral level of 50.

•Most major currencies appreciated against the U.S. dollar in November. Gold also saw positive results, boosted by notable declines in Treasury yields.

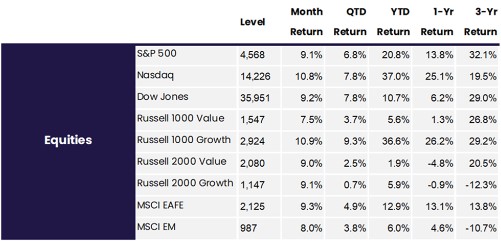

Equities

•Bottom-up 2023 EPS estimates for the S&P 500 moved up to $221 in November from $220 previously, while top-down strategist estimates were revised up to $222 from $219.

•The S&P 500 snapped its three-month losing streak, having its best month of returns since July 2022.

•While small-cap value and growth stocks had similar performance in November, large-cap value stocks outperformed their growth counterparts by 3.4 percentage points.

•Energy was the only sector with negative returns in November, weighed down by the 6.2% decline in oil prices.

Fixed Income

•10-year Treasury yields declined by 60bps in November, the largest single-month decline since December 2008.

•The total investment grade U.S. bond market had its best month since the 1980s, returning 4.5%.

•After beginning the month at 466bps, HY bond spreads declined to 409bps, the lowest since May 2022.

Landing Gears Extended

Most measures of inflation have come down, which is good news. That they have come down while growth and employment have remained resilient is great news. In fact, not only has core PCE inflation trended down and come in lower than the Fed’s September estimate from its Summary of Economic Projections (SEP), it has undershot what the central bank projected in each of the last four SEPs.

Simply assuming that a trend will continue because the line on a chart has been going down steadily is not a reliable approach, but there are some reasons to expect it might. For example, the NY Fed’s Global Supply Chain Pressure index has continued to fall and is at its lowest level since at least 1997, wholesale used car prices continue to plunge, and muted market rent trends appear to finally be showing up in the official data. While not comprehensive, these factors suggest that there’s more disinflation in the pipeline.

These developments have led to a growing consensus of soft landing calls, but risks remain and we view a soft landing as less likely than consensus would suggest. What does seem certain, however, is that the runway to land the economy is coming into view. We’ll soon find out how it goes.

The Name’s Bond, US Bond

Excitement at the prospect of getting inflation down to target without job losses or recession has certainly driven strong performance of major asset classes: The S&P 500 had its ninth best month since 1990, while the investment grade U.S. bond market return of 4.5% ranks as its best month over the same period. A big contributor to the move was the decline in Treasury yields, with 5-year maturities and beyond seeing yields fall by 59-61bps, while shorter maturities moved less. This sort of shift in the yield curve is called a bull flattener and it tends to be good for bonds. November was no exception.

Stocks having such a strong month is a bit more of a surprise when looking through a traditional economic lens. Longer-term yields usually decline when investors think interest rates are too restrictive and become fearful that economic weakening lies ahead. That, in turn, usually results in weaker growth and earnings, which puts pressure on stock prices.

While we’ve in fact seen a slowdown in some of the data, investors haven’t yet seen enough to worry. For now, the economy is cooling at a comfortable pace, but every hard landing looks like a soft landing at first. Markets currently seem to be priced for avoiding a hard landing, but if one does materialize, the risks of a drawdown remain.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.