Navigating the Maze: Unraveling Contradictions in 2024’s Investing Landscape

Estimated reading time: 0 minutes

Unraveling the Enigma

Wrapped in Contradictions. It would be too easy and too obvious if all the signals said the same thing. But the opposite extreme isn’t fun either, the plethora of counterpoints for every point can leave investors with their heads spinning. And that’s where I think we are right now, wrapped in contradictions.

If 2023 was so unpredictably positive, what will 2024 bring?

Since so much of investing is based on an uncertain future, it’s important to focus on more concrete data when and where possible. One of those datasets is the ISM Manufacturing Purchasing Managers Index (PMI). The nice thing about this index is we have a clear threshold of “good” or “bad”. Any reading below zero in the chart signals contraction, anything above zero signals expansion. The Manufacturing PMI has been squarely in contraction territory since late 2022.

The Great Debate

But this is one of those very debatable points, with the counterpoint being that a manufacturing PMI in contraction does not always result in recession. Additionally, the services PMI isn’t in contraction, and our economy is more dependent on services than manufacturing. Both of those points would be true. And the counterpoints in response would be: More often than not, prolonged contractions in manufacturing PMI are coupled with recessions, services PMI did briefly dip into contraction in December 2022, and recessions have happened when services very briefly dipped into contraction (e.g., 2020).

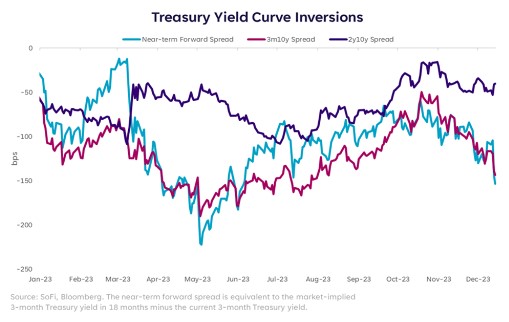

Unveiling the Haunting Yield Curve Inversions

See the conundrum of contradictions? Some of the data is more difficult to contradict, however. And that’s the data that keeps me up at night, the pieces that can’t be ignored. One piece that has haunted me all year, and will continue to haunt me into 2024 are the deep and persistent yield curve inversions.

There’s not just a curve inversion in one place, the curves are inverted in all of the cases illustrated above, and have been for over a year. These aren’t minor inversion either, they’re indisputable, and lasting inversions that send a signal of lower short rates in the near-to-medium term.

The only thing to debate is why short rates would come down (i.e., why the Fed would cut rates). Will they be able to start cutting rates to simply normalize policy? Or will they start cutting rates because economic data cooled too quickly and concerns over a contraction were mounting? Or worse, because of some sort of event that risks spreading into other parts of capital markets?

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.