May 2024 MARKET LOOKBACK

Estimated reading time: 6 minutes

Animal spirits carried the stock market to a new all-time high in May. Risk sentiment returned in a big way in May, with stock indexes setting new all-time highs. Economic data came in mixed, as the latest nonfarm payrolls report showed fewer jobs added than expected while some inflation data remained hot. The latest batch of earnings continued the recent trend of strong beats, with profit margins in particular coming in above expectations. Federal Reserve officials indicated that they were not in a rush to cut interest rates, and would need to see further progress on inflation before doing so. Treasury yields were volatile in response to the mix of economic data and Fed commentary, initially declining before retracing higher during the second half of the month.

Macro

- The FOMC held the fed funds target rate at a range of 5.25%-5.50% and announced they would slow the pace of balance sheet runoff.

- Federal Reserve officials indicated that they would need to see several more months of solid inflation data before they would gain the confidence to lower interest rates.

- 175k nonfarm jobs were added in April, notably below the estimate of 240k, while the unemployment rate ticked up from 3.8% to 3.9%.

- April PPI surprised to the upside at 0.5% m/m and 2.2% y/y, yet CPI came in slightly below consensus at 0.3% m/m and 3.4% y/y.

- The March ISM Manufacturing PMI came in above estimates at 50.3, while the Services PMI was below estimates at 51.4. Both indexes measured above the neutral threshold of 50.

- Homebuilder sentiment declined from an index value of 51 to 45 (i.e. below the neutral 50).

- The Dollar Index, which tracks the strength of the U.S. dollar against a basket of major currencies, weakened from a value of 106.2 to 104.7 in May.

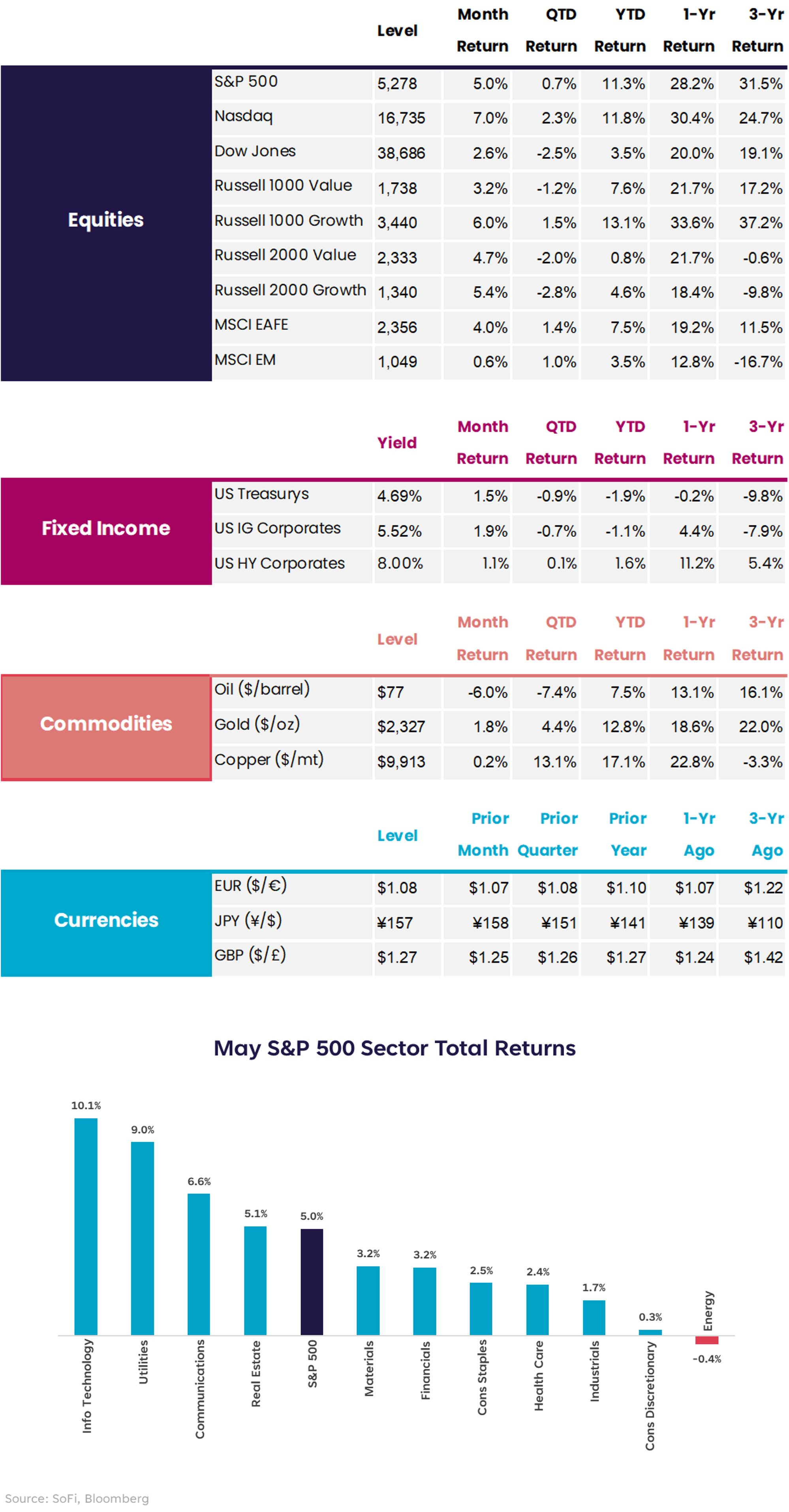

Equities

- Buoyed by mega-cap tech companies, the Nasdaq returned 7.0% in May, its best month since November.

- Bottom-up 2024 EPS estimates for the S&P 500 rose from $243 to $245 in May, while top-down strategist estimates rose from $246 to $247.

- Growth stocks outperformed value stocks by 2.7 percentage points.

- Emerging market stocks lagged the S&P 500 by 4.4 percentage points, reversing last month’s 4.5 percentage point outperformance.

- Weighed down by the slump of oil prices, the Energy sector was the only sector to post a negative return.

Fixed Income

- Treasury yields fell 30-40bps through mid-May, before rising 15-20bps over the second half of the month.

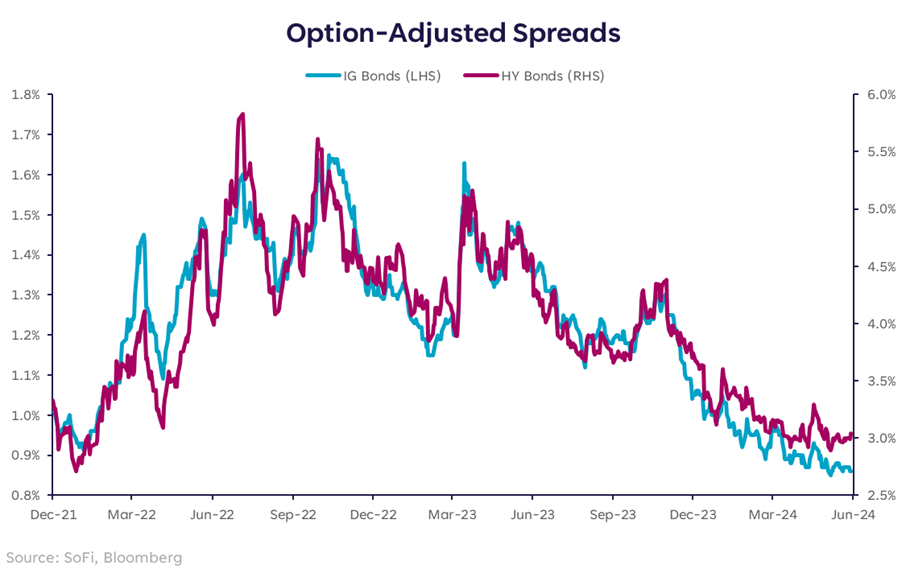

- Credit spreads were relatively unchanged in May, remaining at two-year lows.

- Due to their lower duration (i.e. sensitivity to changes in interest rates), high yield bonds underperformed investment grade bonds and Treasurys.

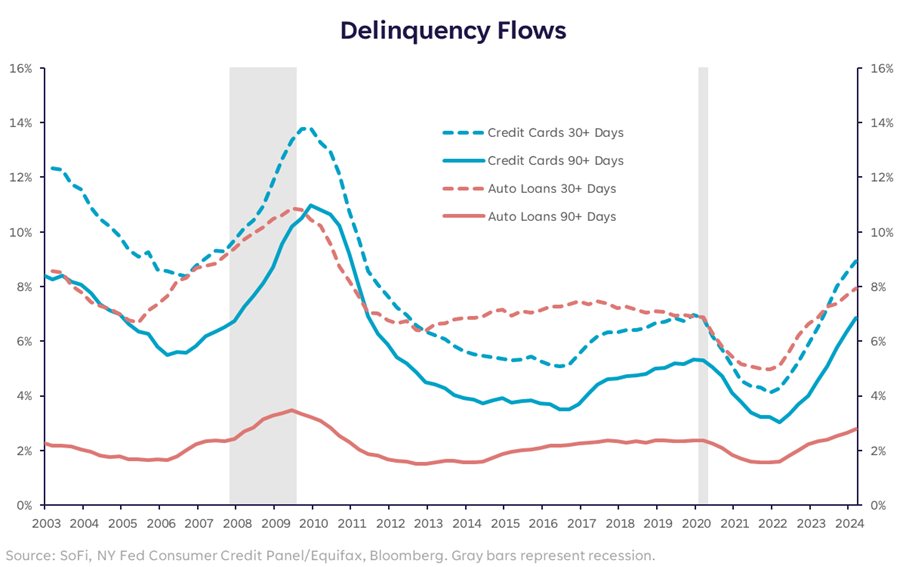

Debts Are Coming Due

A common refrain over the last year or two has been that the strength of the economy continues to surprise. Despite one of the most aggressive hiking cycles in decades, not only did a recession not materialize, but economic growth remained persistently above-trend. Still, there are some concerning signs in pockets of the economy.

On May 14, the Federal Reserve Bank of New York released its Quarterly Report on Household Debt and Credit. While it didn’t necessarily have any major bombshells, it showed the continuation of recent consumer debt and delinquency trends, with stress especially apparent in credit cards and auto loans.

Delinquencies in these markets have risen largely unabated since 2021 and now are around 2011 levels. That’s not totally surprising considering where borrowing costs are now versus then, but what is surprising is that the unemployment rate is below 4% now versus around 9% then.

The solid labor market has helped support consumers and the broader economy, but even that trajectory has been gradually changing. If this labor cooling were to turn into meaningful layoffs, delinquency trends could snowball into something far worse.

Extra Credit

Investors have taken this data in stride, and continue to be sanguine when it comes to the state of the economy overall. Look no further than the S&P 500 setting a new all-time high record on May 21 when it hit 5,321.

Beyond the records, it’s notable that the strong month for stocks was driven by improvements in both earnings and valuations: Of the S&P 500’s 5% gain in May, one-third was driven by higher forward earnings expectations, and two-thirds came from a higher P/E multiple.

Interpreting higher earnings expectations is pretty straightforward, while higher valuation multiples indicate investors paying more per dollar of earnings. Why that’s the case is up in the air, but one reason might be that investors judge the risk of market stress to be low. As a result, investors are more confident that earnings projections will come through. The bond market is signaling something similar, with credit spreads at their lowest levels since early 2022, before the Fed started hiking rates.

So, despite the deterioration in some parts of the consumer credit market, investors don’t expect the same for businesses. While market pricing currently points to a benign economic backdrop for now, things can change quickly.

Disclaimer

SoFi Securities (Hong Kong) Limited and its affiliates (SoFi HK) may post or share information and materials from time to time. They should not be regarded as an offer, solicitation, invitation, investment advice, recommendation to buy, sell or otherwise deal with any investment instrument or product in any jurisdictions. Keep in mind that investing involves risk, and past performance of an asset never guarantees future results or returns. It’s important for investors to consider their specific financial needs, goals, and risk profile before making an investment decision.

SoFi HK does not make any warranties about the completeness, reliability and accuracy of this information and will not be liable for any losses and/or damages in connection with the use of this information.

The information and materials may contain hyperlinks to other websites, we are not responsible for the content of any linked sites. The information and analysis provided through hyperlinks to third party websites, while believed to be accurate, cannot be guaranteed by SoFi HK. These links are provided for informational purposes and should not be viewed as an endorsement. The risk involved in using such hyperlinks shall be borne by the visitor and subject to any Terms of Use applicable to such access and use.

Any product, logos, brands, and other trademarks or images featured are the property of their respective trademark holders. These trademark holders are not affiliated with SoFi HK or its Affiliates. These trademark holders do not sponsor or endorse SoFi HK or any of its articles.

Without prior written approval of SoFi HK, the information/materials shall not be amended, duplicated, photocopied, transmitted, circulated, distributed or published in any manner, or be used for commercial or public purposes.

About SoFi Hong Kong

SoFi – Invest. Simple.

SoFi Hong Kong is the All-in-One Super App with stock trading, robo advisor and social features. Trade over 15,000 US and Hong Kong stocks in our SoFi App now.